If you’re earning over $500,000 annually, you aren’t just paying taxes; you’re funding a silent partner who takes up to 40% of your hard-earned capital without contributing a dime to your growth. For many tech executives and business owners, the complexity of multi-state income and sudden AMT exposure from stock option exercises creates a massive tax drag that can erode 25 years of wealth building in a single filing season. It’s time to stop settling for basic compliance and start implementing sophisticated tax saving strategies for high income earners that prioritize wealth preservation over simple reporting.

You’ve likely realized that the traditional CPA approach of looking in the rearview mirror is costing you a fortune in missed opportunities. We agree that your financial success shouldn’t make you a target for institutional inefficiency. This guide provides the definitive 2026 blueprint to help you transition from passive compliance to proactive architecture, utilizing the same institutional-grade frameworks that ultra-high-net-worth families use to protect their legacies. You’ll discover how to engineer a bespoke tax strategy that addresses RSU optimization, multi-entity structuring, and the specific liabilities of high-stakes earners.

Key Takeaways

- Transition from reactive filing to proactive wealth engineering by adopting a “Strategic Architect” framework that anticipates liabilities before they occur.

- Master institutional-grade tax saving strategies for high income earners that leverage sophisticated “above-the-line” deductions and elite retirement vehicles to aggressively optimize your AGI.

- Implement advanced structural engineering, including Charitable Remainder Trusts and multi-entity blueprints, to defer capital gains and capture maximum QBI deductions.

- Unlock “Investment Tax Alpha” by transforming tax-loss harvesting into a systematic strategy while shielding significant equity through the Section 1202 QSBS exclusion.

- Discover the exclusive blueprint designed to help you win the war for money and success through a bespoke, white-glove approach reserved for fewer than 1,000 elite clients.

The Strategic Architect Approach: Why Compliance Is Not a Tax Strategy

Stop looking in the rearview mirror. Most high earners treat tax season as a post-mortem exercise where they hand over a stack of K-1s and 1099s to a CPA who simply records history. This isn’t a strategy; it’s a compliance autopsy. To protect your wealth in a shifting legislative environment, you must adopt the mindset of a Strategic Architect. We don’t just report numbers. We engineer structural blueprints that minimize tax drag and maximize long-term preservation. This proactive engineering is the only way to ensure your capital works as hard as you do.

Winning the war for money requires institutional-grade precision. Standard tax software isn’t designed to handle the friction of complex compensation packages, multi-state footprints, or concentrated stock positions. Without a proactive framework, you’re effectively volunteering a massive portion of your growth to the Treasury. Implementing robust tax saving strategies for high income earners is about moving from defensive filing to offensive optimization. It’s the difference between following the rules and mastering the system to ensure your legacy remains intact.

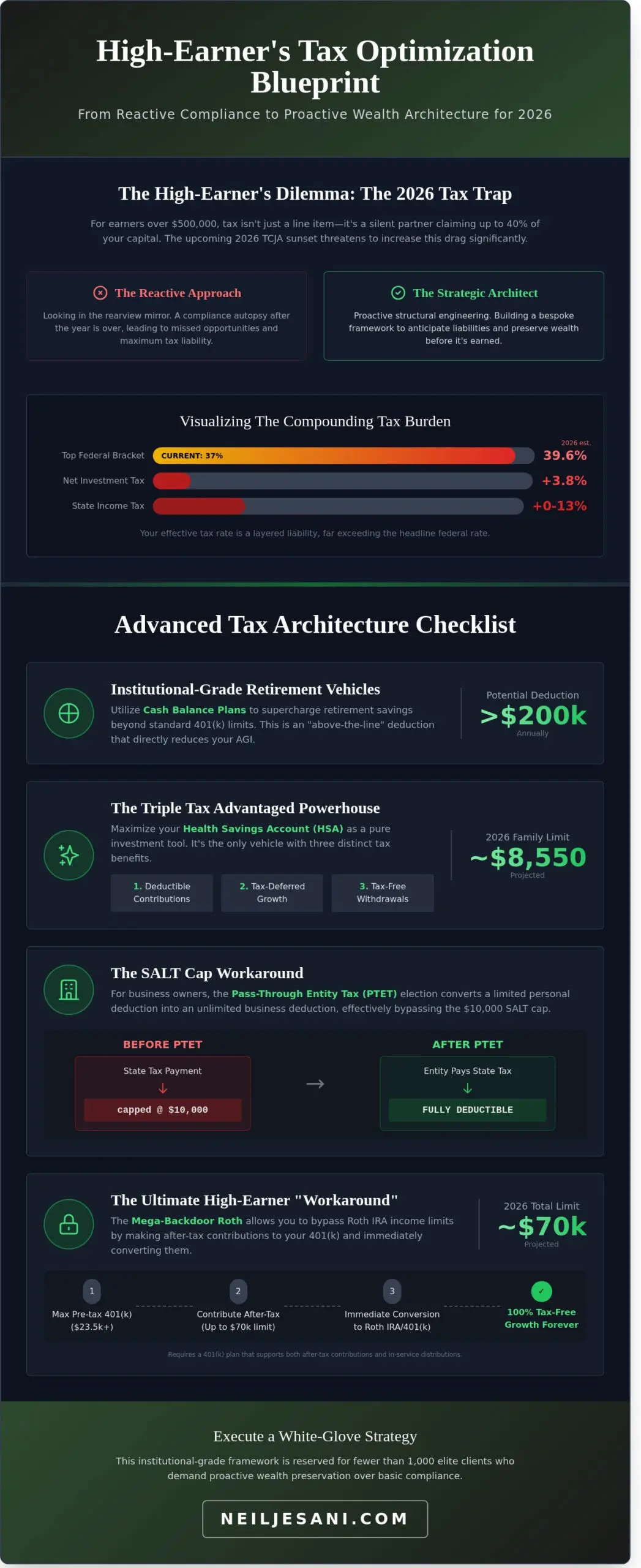

The 37% Trap: Understanding Your Real Tax Liability

High-income earners often underestimate their total effective liability. While the top federal bracket sits at 37% currently, the January 1, 2026, sunset of the Tax Cuts and Jobs Act (TCJA) threatens to push that rate back to 39.6% for individuals earning over $400,000. This doesn’t account for the 3.8% Net Investment Income Tax (NIIT) or the loss of various itemized deductions. For those earning above $500,000, these layers create a compounding drain on capital. A white-glove advisory service is a mathematical necessity to prevent wealth erosion before the bill arrives.

Beyond Filing: The Proactive Planning Lifecycle

April 15th is a deadline for the past, but you build true wealth in the other 364 days of the year. Proactive planning involves constant adjustments to legislative shifts and market volatility. The upcoming 2026 changes require immediate structural pivots to your trusts and entities to avoid being caught in the transition. Neil Jesani serves as the elite tactician for this high-stakes environment, moving beyond simple compliance to design bespoke frameworks. We ensure your tax saving strategies for high income earners are as dynamic as the markets themselves, ensuring you stay ahead of the curve and keep what you’ve earned.

The Advanced Deduction Checklist: Optimizing Your AGI in 2026

Standard tax prep looks in the rearview mirror; elite wealth engineering looks through the windshield. If your current advisor only talks about standard 401(k) limits, you’re leaving millions on the table over a decade. To master tax saving strategies for high income earners, you must move beyond simple compliance and into the active structural optimization of your Adjusted Gross Income (AGI).

Your 2026 blueprint should prioritize institutional-grade vehicles like Cash Balance Plans, which allow for additional deductions often exceeding $200,000 depending on your age and income levels. Don’t overlook the Health Savings Account (HSA) as a pure investment tool. For 2026, projected family contribution limits reach approximately $8,550. This is the only vehicle offering a triple tax advantage: tax-deductible contributions, tax-deferred growth, and tax-free withdrawals for medical expenses. High-revenue business owners must also leverage the Pass-Through Entity Tax (PTET). This strategy allows you to pay state taxes at the entity level, effectively bypassing the $10,000 SALT cap and converting a non-deductible personal expense into a fully deductible business expense.

Retirement Engineering: Backdoor and Mega-Backdoor Roths

The Mega-Backdoor Roth remains the ultimate “workaround” for high-income W-2 earners who exceed standard Roth IRA income limits. In 2026, the total defined contribution limit under Section 415(c) is expected to hover around $70,000. By making after-tax contributions beyond your $23,500 elective deferral and immediately converting them, you shield significant capital from future capital gains taxes. You must verify your plan supports “in-service distributions” and “after-tax non-Roth contributions” before executing this maneuver. You can analyze your plan’s architecture to ensure these features are enabled for maximum wealth acceleration.

Charitable Architecture: DAFs and Private Foundations

Strategic philanthropy is a precision tool for AGI reduction. Donor Advised Funds (DAFs) offer an immediate tax deduction for the full fair market value of appreciated assets, up to 30% of AGI, while allowing you to distribute the funds over time. For those seeking to manage $5 million or more in charitable capital, a Private Foundation provides greater control over legacy and family employment. We often recommend “bunching” three to five years of charitable contributions into a single tax year. This ensures you exceed the projected $30,000 standard deduction threshold, maximizing your itemized benefits while the assets grow tax-free within the DAF structure. This approach allows you to win the war for money and success by turning a social obligation into a sophisticated tax hedge.

Structural Wealth Engineering: Trusts and Multi-Entity Planning

Winning the war for money and success requires more than just filing forms; it demands a rigorous blueprint for your balance sheet. Most high-earners treat their tax bill as an inevitable expense. We treat it as a variable to be engineered. By deploying sophisticated tax saving strategies for high income earners, we move beyond simple deductions into the world of structural optimization. This is where we separate the wealthy from the merely well-paid.

Charitable Remainder Trusts (CRTs) act as a powerful release valve for capital gains. If you’re holding highly appreciated assets with a low cost basis, a CRT allows you to sell those assets, defer the tax hit, and create a lifetime income stream. It’s a surgical strike against the 20% capital gains rate and the 3.8% Net Investment Income Tax. Meanwhile, K-1 engineering allows us to shift income through a multi-entity framework. This ensures every dollar lands in the most favorable tax environment possible, often shielding it from the highest individual brackets.

Trust Architecture for High-Net-Worth Families

Strategic Architects use Irrevocable Life Insurance Trusts (ILITs) to remove death benefits from the taxable estate, providing liquidity without the 40% tax haircut. To combat the 2026 sunset of current gift tax exemptions, we implement Intentionally Defective Grantor Trusts (IDGTs). These tools freeze the value of your estate at today’s prices, allowing all future growth to pass to heirs tax-free. Our white-glove process ensures your legal counsel and tax strategists operate from the same playbook to avoid costly structural cracks.

Business Entity Optimization for 2026

The 20% QBI deduction under Section 199A is scheduled to expire on December 31, 2025. This makes your choice of entity for 2026 a high-stakes decision. While S-Corps offer self-employment tax savings, a C-Corp might provide a superior flat 21% rate if the QBI deduction vanishes. We analyze your specific cash flow to determine if a Family Limited Partnership (FLP) can provide the valuation discounts needed for aggressive asset protection. Consider this your entity-level checklist:

- Review Section 1202 eligibility for 100% gain exclusion on Qualified Small Business Stock.

- Analyze the “S-Corp vs. C-Corp” math specifically for the post-2025 tax environment.

- Validate that all inter-company management fees meet the “reasonable” standard to withstand IRS scrutiny.

- Finalize all entity-level tax elections before the March 15 deadline to maintain maximum flexibility.

Asset protection isn’t just about lawsuits. It’s about shielding your hard-earned capital from the “tax drag” that erodes institutional-grade wealth over decades. We don’t just help you survive the tax season; we help you dominate it.

Investment Tax Alpha: Harvesting Gains and Shielding Equity

Stop viewing tax-loss harvesting as a year-end cleanup. It’s a systematic engine for wealth preservation. For the elite investor, “alpha” isn’t just market outperformance; it’s the spread between your gross return and what you actually keep. High-earners often lose 40% or more of their annual growth to tax drag. We engineer portfolios to capture losses in real-time, creating a bank of offsets that shield future gains. This proactive approach includes integrating low-correlation alpha, using alternative assets that don’t move with the S&P 500 to stabilize returns while maximizing net-of-tax results. This isn’t just accounting. It’s an institutional-grade strategy to ensure your wealth grows without unnecessary leakage.

Managing Concentration Risk and RSU Taxation

Tech executives and founders often find their wealth trapped in a single ticker symbol. This concentration risk is a ticking time bomb. Effective tax saving strategies for high income earners require a proactive blueprint for equity compensation. If you’re at an early-stage firm, the 83(b) election is your most powerful weapon. Missing that 30-day window can cost millions in future capital gains. For those with RSUs, we often recommend a “sell-on-vest” protocol to diversify immediately; there’s rarely a tax advantage to holding shares with a zero-cost basis once they’ve hit your account.

- Model AMT exposure before exercising ISOs to avoid paying tax on “phantom” gains you haven’t realized.

- Utilize zero-cost collars to hedge downside risk on concentrated positions without triggering a Section 1259 constructive sale.

- Maintain a 10b5-1 trading plan to provide legal cover while systematically reducing exposure to a single asset.

The QSBS Windfall: Protecting Your Exit

Section 1202 is the ultimate prize in the tax code. If your stock qualifies as Qualified Small Business Stock (QSBS), you can exclude 100% of the gain from federal taxes, up to $10 million or 10 times your basis. However, the IRS is increasingly aggressive in auditing these claims. You must document that the company met the 80% active asset test throughout your entire five-year holding period. To maximize this, we use “stacking” and “packing” techniques. This involves utilizing non-grantor trusts to multiply the $10 million exclusion across multiple family members or entities. This is how we move beyond simple filing to true wealth architecture.

Don’t leave your exit to chance. Engineer your wealth preservation strategy with our elite team today.

The Neil Jesani Blueprint: Winning the War for Money and Success

Most financial plans are built for the past. They focus on what you earned last year rather than what you will keep in 2026. The Strategic Architect framework flips this script by treating your wealth as a high-performance engine that requires precise calibration. We don’t just offer advice; we engineer outcomes through a rigorous, institutional-grade process. By limiting our firm to fewer than 1000 clients, we ensure that every high-net-worth individual receives the aggressive advocacy and meticulous attention required to win the war for money and success.

Our approach integrates fractional CFO services with sophisticated tax saving strategies for high income earners. This synergy allows us to look at your ISOs, RSUs, and multi-entity structures through a single, unified lens. We treat tax planning as a year-round offensive maneuver rather than a seasonal administrative chore. When your tax strategy is decoupled from your business growth, you lose money. We bridge that gap to ensure every dollar is working toward your legacy.

The White-Glove Experience: What to Expect

Onboarding at Neil Jesani isn’t a simple paperwork exercise. It’s a comprehensive tactical briefing. Our team of 70+ professionals, including veteran CPAs and elite attorneys, work in unison to audit your current exposure. We analyze your K1s and AMT exposure with a level of technical precision that standard firms can’t match. This collaborative environment ensures that your legal protections and tax maneuvers never contradict one another.

Our commitment is defined by the “Beyond Filing” promise. While others focus on compliance, we focus on growth. We provide a proactive roadmap that anticipates shifts in tax law, ensuring your wealth preservation strategy remains resilient against political or economic volatility. You aren’t just hiring a firm; you’re gaining a command center for your financial life.

Your Next Strategic Move

An elite tax strategy partnership isn’t for everyone. We specifically partner with individuals who recognize that tax is their largest recurring expense and are ready to stop being a silent partner to the IRS. If you manage a complex portfolio or lead a high-growth enterprise, you can’t afford a reactive accountant who only looks in the rearview mirror. Our tax saving strategies for high income earners are designed for those who demand excellence and refuse to accept the status quo of “standard” deductions.

Stop settling for traditional wealth management that was built for a different era. It’s time to deploy a bespoke framework that protects your capital and accelerates your success. Take the first step toward institutional-grade wealth defense today.

Ready to engineer your financial future?

Stop Reacting and Start Engineering Your Wealth

Waiting until April to think about your taxes isn’t a strategy; it’s a surrender. To protect your capital in 2026, you must shift from simple compliance to structural wealth engineering. This means optimizing your AGI through advanced deductions and shielding equity with multi-entity planning. Real tax alpha isn’t found in a standard software program. It’s built through a bespoke framework that integrates tax planning with institutional-grade wealth management. You’ve worked too hard to let tax drag erode your legacy.

Our firm provides the specialized tax saving strategies for high income earners that traditional CPAs often overlook. We maintain a team of 70+ members with over 200 years of combined expertise to ensure your blueprint is flawless. We limit our practice to fewer than 1,000 clients to guarantee a true white-glove experience. It’s time you had an ally who understands that wealth preservation is a high-stakes mission. You deserve a partner who helps you win the war for money and success.

Take command of your financial future today. Join the Elite: Schedule Your Bespoke Tax Strategy Session and start building your 2026 defense. You’ve built the empire; now let’s make sure you keep it.

Frequently Asked Questions

What is the most effective tax saving strategy for W-2 earners making over $500k?

The most effective method for W-2 earners over $500,000 involves utilizing private equity investments in energy or equipment leasing that qualify for Section 179 deductions. These tax saving strategies for high income earners can offset up to 100% of your active income, moving you out of the 37% top bracket immediately. It’s not about simple 401k contributions; it’s about engineering active losses to shield your high-stakes earnings from federal erosion.

How does the 2026 tax law change affect high-income earners?

On January 1, 2026, the sunset of the Tax Cuts and Jobs Act will trigger a mandatory increase in the top marginal rate from 37% to 39.6%. Additionally, the lifetime estate tax exemption is projected to drop by 50%, falling from $13.61 million to roughly $7 million per individual. You must restructure your holdings now to avoid a massive wealth transfer to the government when these 2017 provisions expire.

Can I still use a Backdoor Roth IRA if I exceed the income limits?

You can absolutely use a Backdoor Roth IRA regardless of your income level, provided you follow the specific two-step conversion process. For 2024, the income phase-out starts at $146,000 for individuals, but the “backdoor” allows you to bypass this by making a non-deductible contribution. It’s a critical component of a bespoke wealth blueprint that ensures your future growth and distributions remain 100% tax-free for life.

What is the difference between tax compliance and advanced tax strategy?

Tax compliance is the administrative task of reporting what happened last year, while advanced tax strategy is the proactive architecture of your future wealth. Most CPAs spend 90% of their time looking in the rearview mirror to meet April 15 deadlines. Our elite approach flips the script, focusing on multi-entity structuring and low-correlation alpha to reduce your 37% tax drag before the tax year even begins.

How does a Charitable Remainder Trust (CRT) work for capital gains?

A Charitable Remainder Trust allows you to defer capital gains taxes on the sale of a $1 million asset while securing an immediate income tax deduction. By transferring the asset to the trust before the sale, you avoid the 20% federal capital gains hit and the 3.8% net investment income tax. It’s a sophisticated framework for those looking to build a legacy while maintaining a 5% to 7% annual payout.

What are the benefits of a fractional CFO for a high-revenue business owner?

A fractional CFO delivers institutional-grade financial strategy for businesses with $10 million in revenue at a fraction of the $350,000 cost of a full-time hire. They don’t just balance books; they optimize your capital stack and manage complex K1 distributions. This level of oversight is essential for business owners who want to scale while maintaining a lean, high-performance corporate architecture that survives an IRS audit.

Is it possible to legally reduce my tax bill by 30% or more?

Reducing your tax bill by 30% or more is legally achievable through the implementation of advanced tax saving strategies for high income earners like captive insurance or R&D credits. For a household earning $1.5 million, these bespoke strategies can save over $450,000 annually. We don’t guess or hope for the best; we engineer a blueprint that uses the existing tax code to protect your capital from unnecessary erosion.

Why do I need an elite advisory firm instead of a local CPA?

An elite advisory firm provides a white-glove experience that a local CPA, who might handle 2,000 small files, simply cannot match. We limit our practice to fewer than 1,000 clients to ensure your wealth architecture receives the technical precision it deserves. You need a strategist to help you win the war for money and success, not just a bookkeeper who records your losses after they’ve already occurred.