Is your current CPA still looking through the rearview mirror while the December 31, 2025, tax cliff approaches? Most high-earners are currently trapped in a reactive cycle, watching helplessly as a 40% tax drag erodes their investment growth year after year. You need more than a historian; you need a tactician. Implementing sophisticated tax planning strategies today is the only way to ensure you don’t lose your hard-earned capital to the 2026 rate hikes. Waiting until the filing deadline is a strategy for the average, not the elite.

You’ve likely felt the frustration of receiving a massive tax bill that could’ve been avoided with proactive foresight. It’s an exhausting way to manage a legacy, especially when you’re trying to win the war for money and success. This guide promises to elevate your financial framework from basic compliance to institutional-grade architecture. We’ll provide a proactive 3 to 5 year roadmap that integrates tax optimization with bespoke wealth management. You’ll discover how to engineer a blueprint that provides total peace of mind while securing your family’s future against shifting legislative tides.

Key Takeaways

- Shift your perspective from retrospective tax filing to forward-looking engineering that treats your financial future as a blueprint rather than a history lesson.

- Learn how to optimize multi-entity structures and equity compensation like RSUs and ISOs to ensure your wealth is built on a foundation of institutional-grade efficiency.

- Identify the critical “CPA Gap” by implementing advanced tax planning strategies that go beyond basic compliance to protect millions in potential savings.

- Discover how to stress-test your multi-year projections and re-evaluate estate planning vehicles before the 2026 exemption cliff threatens your legacy.

- Explore the elite “white-glove” approach to wealth management designed to help high-net-worth individuals win the war for money and success through proactive, bespoke advocacy.

Beyond Compliance: Why Strategic Architecture Trumps Traditional Tax Filing

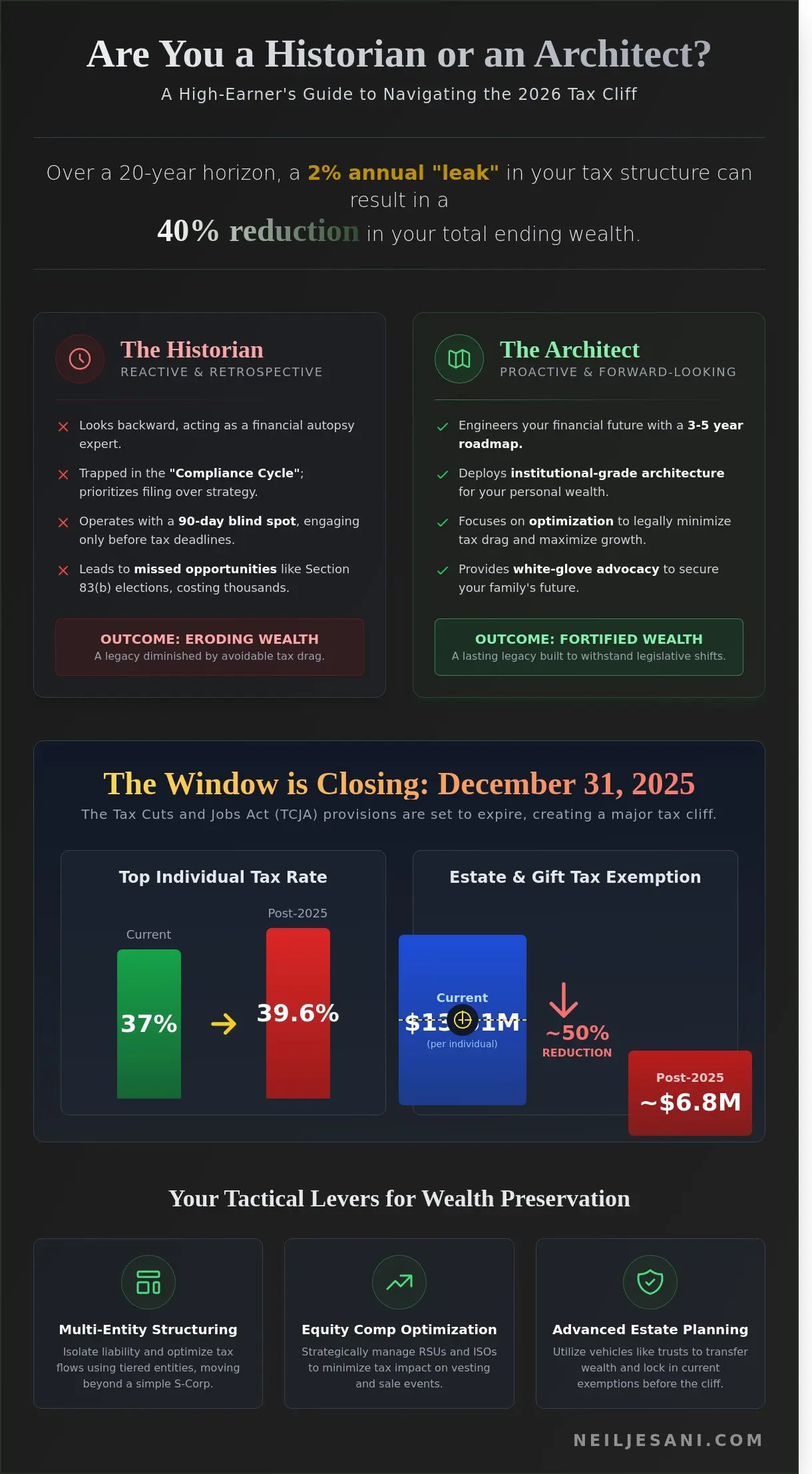

Most high-net-worth individuals treat tax season like a financial autopsy. They hand over a box of receipts to a CPA and wait to see how much they owe for a year that’s already finished. This is retrospective compliance, not strategy. Advanced tax planning is a forward-looking engineering process. It’s the difference between recording history and creating it. While a standard CPA acts as a reactive historian, a strategic architect functions as an elite advisory partner who designs your financial future before the first dollar of income is even realized.

The primary enemy of long-term wealth isn’t the market; it’s tax drag. When you lose 37% to 50% of your earnings to federal and state authorities every year, you’re not just losing cash. You’re losing the compounding power of that capital. Over a 20-year horizon, a 2% annual “leak” in your tax structure can result in a 40% reduction in your total ending wealth. To stop this bleed, you need to move toward the legal use of the tax regime to protect your assets. We bring institutional-grade planning, the kind of sophisticated multi-entity structuring usually reserved for Fortune 500 corporations, to the private citizen’s balance sheet. It’s time to win the war for money and success by treating your wealth like a fortress.

The Cost of Reactive Planning

Relying on a traditional CPA often leads to the “Compliance Trap.” The Compliance Trap is the tendency to prioritize the administrative act of filing over the proactive execution of strategy. Your current professional is likely obsessed with “not getting audited,” which sounds safe but is actually a defensive crouch that costs you millions. Missing a single Section 83(b) election or failing to time an RSU vest correctly can cost a tech executive $150,000 in a single high-income year. If your advisor isn’t looking at your 2027 liability today, they’re already behind the curve. Tax planning strategies must be engineered with a three-to-five-year lead time to be truly effective.

- Audit Fear vs. Optimization: Defensive filing ignores legal deductions that require complex documentation.

- The 90-Day Blind Spot: Most CPAs only talk to you during the 90 days before April 15.

- Structural Rigidity: Reactive planning fails to account for shifting income brackets or state residency changes.

The 2026 Horizon: Preparing for the Sunset

The clock is ticking on the most favorable tax environment in recent history. On December 31, 2025, the core provisions of the Tax Cuts and Jobs Act (TCJA) are set to expire. This isn’t just a minor adjustment; it’s a structural shift. The top individual tax rate is scheduled to jump from 37% back to 39.6%. More importantly, the lifetime estate and gift tax exemption, currently sitting at $13.61 million per individual, is expected to be cut by approximately 50%. This creates a narrow “tactical window” for wealth transfer and income timing that will close permanently in less than 24 months.

Waiting until 2026 to react to these changes is a recipe for wealth destruction. You need a firm like Neil Jesani Advisors that specializes in engineering portfolios for future law changes rather than just reacting to past ones. By implementing sophisticated tax planning strategies now, you can lock in current exemptions and move assets out of your taxable estate before the window slams shut. This is how the elite preserve their legacies; they don’t wait for the law to change, they architect their wealth to withstand the shift.

Engineering the Blueprint: Core Tax Planning Strategies for 2026

Stop treating your tax return as a post-mortem report. Most high-net-worth individuals view April 15th as the finish line, but for the strategic architect, it is merely a data point in a much larger structural design. By 2026, the sunset of the Tax Cuts and Jobs Act (TCJA) will likely push the top individual tax rate back to 39.6% from 37%. This shift demands aggressive, forward-looking tax planning strategies that prioritize wealth preservation over simple compliance.

We move beyond the elementary S-Corp setup. Elite wealth management requires multi-entity structuring where we utilize tiered entities to isolate liability and optimize K-1 distributions. This isn’t just about moving money; it’s about changing the character of the income itself. We analyze your asset location, ensuring high-growth assets sit in tax-exempt wrappers while placing high-tax, low-growth assets in structures that minimize the annual drag on your net worth.

Execution requires precision. You need to balance your Alternative Minimum Tax (AMT) exposure against capital gains realization to ensure you aren’t accidentally triggering a higher effective rate. While many advisors focus on broad strokes, we implement tactical tax strategies that include precise income timing and loss harvesting to offset the 20% long-term capital gains rate. It’s a game of inches that results in miles of difference for your balance sheet.

Advanced Structuring for Business Owners

For the business owner, the goal is to dismantle the 15.3% self-employment tax burden. We engineer family management companies to shift income to lower-bracket family members or specialized entities, effectively reducing the overall household tax friction. If you’re in tech or manufacturing, we maximize Section 1202 (QSBS) benefits. This allows for an exclusion of up to $10 million in federal capital gains, or 10 times your basis, upon exit. We don’t just build businesses; we design tax-free exits. Integrating asset protection with this entity design ensures your wealth is shielded from both the IRS and external litigants. You can start architecting your financial future by looking at your business as a series of tax-efficient modules rather than a single taxable block.

Equity and RSU Management for Executives

Executives at firms like Nvidia, Apple, or early-stage unicorns often find themselves “paper rich” but tax-trapped. The 83(b) election is your most powerful lever, yet 40% of founders miss the 30-day filing window, turning a potential capital gains play into a massive ordinary income hit. We manage the timing of ISO exercises to stay just below the AMT threshold, preventing a “phantom tax” bill on stock you haven’t even sold yet. For those with concentrated stock positions exceeding 20% of their portfolio, we deploy exchange funds or completion portfolios. These advanced tax planning strategies allow you to diversify without triggering a massive 23.8% tax event (including the Net Investment Income Tax). We don’t hope for a lower bill; we engineer it through disciplined exercise schedules and rigorous cost-basis tracking.

The “CPA Gap”: Why Your Current Professional Might Be Leaving Millions on the Table

“I already have a tax guy.” This phrase is the most common objection we hear, and it’s frequently the most expensive mistake a high-net-worth individual can make. You don’t need a historian to record your losses; you need a tactician to engineer your wins. Most tax professionals operate as historians. They look through the rearview mirror, documenting what happened last year to satisfy the IRS. This is the “Volume Model.” When a CPA manages 500 or more returns, your financial future receives roughly 15 minutes of attention during the peak of tax season. That isn’t strategy; it’s data entry.

The difference between a tax preparer and a true Tax Strategist is the difference between a bookkeeper and an architect. A preparer fills out forms. A CPA provides a professional opinion on those forms. A Tax Strategist, often backed by Tax Attorneys, builds the multi-entity structures that protect your ISOs, RSUs, and real estate holdings before the tax bill is even generated. If your professional isn’t looking three years ahead, they’re simply recording your wealth’s slow erosion. You’re paying for compliance when you should be investing in optimization.

Identifying the red flags of “maintenance mode” is simple. Does your advisor call you with ideas, or do you call them with questions? If your interaction is limited to a checklist sent in February, you’re trapped in a volume-based relationship. A bespoke model requires a proactive cadence. It demands an advisor who understands that a 30% tax drag on a $10 million portfolio isn’t just a bill; it’s $3 million of lost compounding power over time. Elite wealth management requires a forward-looking blueprint, not a yearly autopsy of your bank account.

This principle holds true regardless of location; finding a dedicated, client-focused firm is key. For example, a boutique practice like Cairns Quality Accounting can provide the personalized tax services that larger, volume-based operations often lack.

The Myth of the Comprehensive CPA

Most CPAs are buried under 500+ tax returns, leaving them zero capacity for deep-dive tax planning strategies. They focus on compliance rather than optimization. Compliance ensures you don’t go to jail; optimization ensures you keep your hard-earned capital. There’s a massive legal chasm between tax avoidance, which is the strategic use of the code to your advantage, and tax evasion. If your current advisor hasn’t analyzed how the 2026 sunsetting of the Tax Cuts and Jobs Act affects your specific estate, they aren’t planning. They’re just filing. You should audit your advisor by their ability to reduce your effective tax rate, not the size of your refund check.

The Power of a Collaborative In-House Team

Siloed advice is the silent killer of private wealth. Your CPA doesn’t talk to your estate attorney; your wealth manager doesn’t understand your K1 complexities or your AMT exposure. This lack of coordination creates strategic leakage where opportunities vanish. We solve this by putting CPAs, Tax Attorneys, and Wealth Managers in one room to stress-test your tax planning strategies. This institutional-grade approach ensures your RSU exits and multi-entity structures work in total harmony.

We bridge those gaps to help you win the war for money and success.

Tactical Levers for 2026: A High-Net-Worth Action Plan

The 2026 tax cliff isn’t a theory. It’s a scheduled collision for every individual with a net worth exceeding $10 million. If you’re waiting for a legislative miracle to extend the Tax Cuts and Jobs Act (TCJA) provisions, you’re already behind. Winning the war for money and success requires an offensive tax planning strategies framework that moves beyond annual compliance into multi-year engineering.

Step 1: Conduct a 36-Month Stress Test. Stop looking at your tax liability in one-year silos. We run simulations that project your cash flow and tax drag through 2027. This reveals exactly how the sunset of lower brackets and the 20 percent 199A deduction will erode your liquidity. If your current CPA hasn’t modeled your 2026 exposure, your blueprint is flawed.

Step 2: Secure Your Estate Exemption. The current federal gift and estate tax exemption sits at $13.61 million per individual. On January 1, 2026, this figure is projected to plummet to approximately $7 million. You’ve a narrow window to move assets out of your taxable estate while retaining institutional-grade control over your family’s future.

Step 3: Execute the “Bunching” Maneuver. We analyze your charitable and business expenses to identify opportunities for acceleration. By grouping three years of planned giving or equipment purchases into the 2025 tax year, you maximize deductions against today’s higher thresholds before the standard deduction and rate structures shift. It’s about timing your outflow to match the highest possible tax benefit.

Step 4: Engineer Advanced Retirement Vehicles. For business owners, a standard 401(k) is a starter tool. We implement bespoke Cash Balance Plans that allow for contributions exceeding $250,000 annually, depending on age and income. This creates an immediate, massive deduction while accelerating your path to a work-optional lifestyle through high-level tax planning strategies.

Estate and Gift Tax Optimization

Locking in the $13.61 million exemption requires sophisticated vehicles like Spousal Lifetime Access Trusts (SLATs) or Grantor Retained Annuity Trusts (GRATs). These structures allow you to freeze asset values today and pass all future appreciation to heirs tax-free. Waiting until December 2025 is a recipe for strategic failure. Appraisal firms and elite legal counsel will have six-month backlogs by then; you must initiate these transfers now to ensure they’re bulletproof. We also utilize high-cash-value life insurance to provide immediate liquidity, ensuring your heirs aren’t forced to liquidate assets to pay a 40 percent tax bill.

Maximizing Business Deductions

Elite earners use the “Augusta Rule” (Section 280A) to rent their primary residence to their corporation for up to 14 days a year. This creates a legitimate business deduction for the entity while providing tax-free income to the individual. For those with complex risk profiles, we explore captive insurance structures to turn premiums into tax-efficient reserves. You can optimize these operations by integrating Fractional CFO services to ensure every tactical play is executed with technical precision. This isn’t just accounting; it’s operational excellence designed to protect your bottom line.

Don’t let the 2026 sunset erode your hard-earned legacy. Schedule your elite tax architecture briefing today to secure your wealth before the window closes.

Win the War for Wealth: The Neil Jesani White-Glove Experience

You aren’t looking for a standard tax preparer; you’re searching for a commander. The financial landscape heading into 2026 is a battlefield. With the Tax Cuts and Jobs Act (TCJA) provisions scheduled to sunset on December 31, 2025, the margin for error has vanished. Our “Win the War for Money and Success” brand philosophy isn’t just a slogan. It’s a proactive mandate. We recognize that for the ultra-high-net-worth individual, wealth isn’t just about what you earn. It’s about what you defend. We don’t just record history; we engineer the future by treating your balance sheet as a high-stakes mission that requires a superior tactician.

The “White-Glove” promise is our commitment to an intensely selective, high-touch partnership. While traditional firms chase volume and scale, we do the exact opposite. We intentionally limit our client base to fewer than 1,000 families. This isn’t just about exclusivity; it’s about capacity. This restriction ensures that every partner receives institutional-grade attention that most retail wealth management firms simply cannot provide. We provide a level of oversight where your “Strategic Architect” is constantly monitoring legislative shifts, ensuring your tax planning strategies are calibrated for the 39.6% top marginal rate and the reduced estate tax exemptions arriving in 2026.

The Bespoke Advisory Framework

We build your wealth preservation plan on a foundation of a 25-year heritage. Our 70+ member team of specialists doesn’t work in silos; they operate as a unified strike team. We combine expertise in multi-entity structuring, RSU optimization, and cross-border tax law to create a multi-year blueprint tailored to your specific legacy goals. During your first Advanced Tax Strategy session, we move beyond the “compliance” mindset. We don’t just look at last year’s K1s. We project your trajectory over the next decade. We analyze your AMT exposure and liquidity events to ensure your wealth remains under your control, not the government’s.

- Institutional-Grade Depth: Access to the same sophisticated structures used by the top 0.1%.

- Proactive Defense: We identify tax “drag” before it hits your bottom line.

- Legacy Engineering: We don’t just save taxes; we design frameworks for multi-generational wealth.

Secure Your Strategic Advantage

Elite earners cannot afford the luxury of waiting for the next tax season. By the time April 15th arrives, the opportunity for meaningful intervention has usually passed. You need a “Strategic Architect” who views your financial life as a dynamic, interconnected system. This partnership provides the peace of mind that comes from knowing every deduction is optimized and every legal loophole is fortified. You’ve spent your life building an empire; it’s time you had a team capable of defending it. Transition from being just another “client” at a massive corporate machine to being a true partner in wealth preservation. Schedule your bespoke tax strategy consultation today and take command of your financial future.

The complexity of the 2026 tax pivot requires more than just a CPA. It requires a firm that understands the intersection of psychology, law, and high-finance. We’ve spent over two decades refining the art of the “White-Glove” experience because we know that at your level, the details aren’t just details. They are the difference between a legacy that thrives and one that is eroded by 40% or more in avoidable taxes. Don’t settle for “standard” when the stakes are this high. Choose the architecture of excellence.

Master Your Financial Architecture Before the 2026 Shift

The 2026 fiscal landscape isn’t just a date on a calendar; it’s a high-stakes deadline for your capital. Most high-earners remain trapped in a cycle of reactive filing that ignores the “CPA Gap” where millions are lost to outdated, compliance-only advice. You need a fundamental shift from administrative paperwork to sophisticated tax planning strategies that function as a rigorous blueprint for wealth preservation. We’ve spent 25 years refining an elite model that protects ultra-high-net-worth individuals from the systemic inefficiencies of standard accounting firms.

Our team of 70 CPAs, tax attorneys, and enrolled agents doesn’t just record your financial history; we engineer your future. By limiting our practice to fewer than 1,000 exclusive clients, we ensure every strategy is a bespoke, institutional-grade masterpiece. You’ve worked far too hard to let a lack of tactical foresight erode your family’s legacy. It’s time to flip the script and win the war for your money with the master plan your success demands.

Secure your institutional-grade tax strategy session today

You’ve built the empire; now let’s build the fortress that keeps it yours for generations to come.

Frequently Asked Questions

How does advanced tax planning differ from standard tax preparation?

Standard tax preparation is a backward-looking compliance exercise that records what happened last year; advanced tax planning is a forward-looking architectural design. Preparation focuses on meeting the April 15 deadline without penalties. Planning analyzes the next 10 years to minimize tax drag through multi-entity structuring and asset location. It’s the difference between reporting a loss and engineering a future gain.

What happens to my tax strategy when the TCJA provisions sunset in 2026?

The sunset of the Tax Cuts and Jobs Act on December 31, 2025, will trigger an automatic increase in the top individual tax rate from 37% to 39.6%. Standard deductions will drop by roughly 50%, and estate tax exemptions will plummet from $13.61 million to approximately $7 million per individual. You must restructure your holdings now to lock in these historically high exemptions before they vanish.

Can W-2 high-earners use the same tax strategies as business owners?

High-income W-2 earners can deploy sophisticated tax planning strategies like Charitable Lead Annuity Trusts or specialized energy investments to offset up to 100% of their taxable income. While business owners focus on K1 distributions, tech executives with heavy RSU income utilize IRC Section 170 deductions. We engineer bespoke frameworks that turn trapped salary into tax-efficient capital for our elite clients.

How much can I realistically save with an advanced tax strategy?

Clients typically realize a 15% to 40% reduction in their effective tax rate through institutional-grade optimization. For a household generating $2 million in annual income, this strategic shift preserves between $300,000 and $800,000 in liquidity every year. These aren’t minor adjustments; they’re structural overhauls designed to maximize your net worth and accelerate your wealth trajectory.

Is advanced tax planning legal and compliant with the IRS?

Every strategy we design relies on specific Internal Revenue Code sections and established tax court precedents to ensure total compliance. We don’t use “grey area” loopholes. Instead, we use the 2,500+ pages of the tax code as a blueprint for efficiency. It’s about following the rules more intelligently than a standard CPA who lacks the time for deep technical research.

What is the “CPA Gap” and how do I know if I am affected by it?

The “CPA Gap” exists when your tax professional spends 95% of their time on historical filing rather than proactive strategy. If your CPA only contacts you in March or April, you’re likely suffering from this gap. You need a strategist who coordinates with your wealth manager to stop the 20% to 30% wealth leakage caused by uncoordinated financial advice.

How do RSUs and ISOs affect my AMT exposure in 2026?

Exercising ISOs can trigger a 26% or 28% Alternative Minimum Tax hit, which becomes more dangerous as TCJA exemptions expire in 2026. Without a blueprint, you might pay taxes on phantom gains if the stock price drops after your exercise. We use 83(b) elections and strategic sell-to-cover schedules to protect your equity and manage this specific tax risk.

Why should I integrate wealth management with my tax planning?

Integrating these disciplines ensures your investment gains aren’t eroded by a 40% tax bill on short-term capital gains. A holistic approach utilizes tax planning strategies like tax-loss harvesting and low-correlation alpha to increase your net returns. It’s the only way to ensure your portfolio growth and tax liability move in opposite directions to secure your family legacy.