Are you hiring a historian to document your financial past, or an architect to engineer your future? Most high-net-worth individuals unknowingly settle for the former. They pay 40% or more in effective taxes while their CPA remains silent until the filing deadline in April. This reactive approach doesn’t just cost money; it leaves millions in potential savings on the table. To fix this, you need the right questions to ask a potential tax advisor to ensure they are a strategist, not just a bookkeeper. You deserve a partner who treats your wealth like a high-stakes battlefield, not a static ledger.

It’s exhausting to realize your current advisor only talks to you once a year. You’ve likely suspected that advanced strategies like multi-entity structuring or RSU optimization are being missed. You’re right to feel that way. To win the war for money and success, you need a tactician who operates with institutional-grade precision. We’ll show you how to identify an elite strategist who provides a proactive tax blueprint rather than a standard preparer who just looks in the rearview mirror. This guide ensures you gain the confidence that no money is being left behind through a bespoke, white-glove advisory relationship where your wealth is engineered, not just recorded.

Key Takeaways

- Stop overpaying for hindsight; discover why a “Strategic Architect” is the only ally capable of engineering your future wealth rather than just recording your past.

- Master the high-stakes questions to ask a potential tax advisor to ensure they are building a forward-looking blueprint rather than simply checking boxes.

- Learn how to stress-test an advisor’s expertise on sophisticated issues like RSU optimization, AMT exposure, and multi-entity structuring for business owners.

- Identify the critical red flags-such as commodity-based pricing-that signal an advisor is ill-equipped to handle an elite, institutional-grade financial profile.

- Discover the “Beyond Filing” model that integrates CPAs, attorneys, and CFOs to flip the script on the tax system and protect your legacy.

Why Most High Earners Hire the Wrong Tax Professional

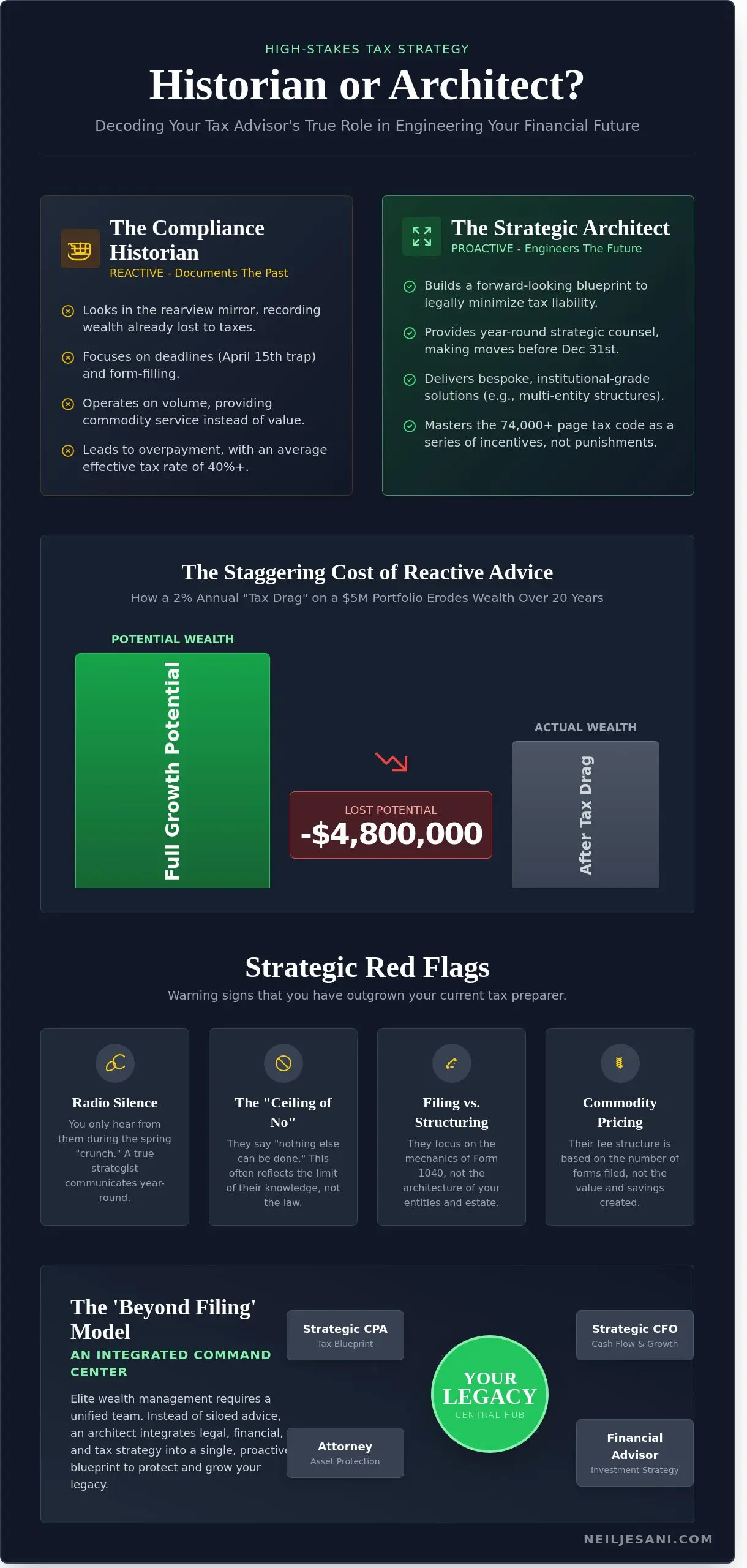

Most high earners mistakenly hire a “Compliance Historian” when they desperately need a “Strategic Architect.” A Compliance Historian spends their time looking in the rearview mirror. They accurately record the wealth you’ve already lost to the government. They focus on the 37% top marginal rate and ensure your forms are signed on time. While this keeps you out of legal trouble, it does nothing to protect your capital from future erosion. You’re effectively paying for an autopsy when you need life-saving surgery to win the war for money and success.

A standard CPA is often your largest hidden expense. They operate within a framework of volume rather than value. If your preparer handles 500 returns in a single season, they don’t have the bandwidth to engineer bespoke solutions for your specific RSU schedule or multi-entity structure. While researching various types of tax professionals, it’s vital to realize that credentials don’t always equal strategy. Most professionals are trained to stay within the lines of the past. They don’t possess the institutional-grade vision to build a blueprint for your future.

The “April 15th Trap” is a primary reason why wealth stagnates. By the time you hand over your documents in March, your financial fate for the previous year is already sealed. You’re simply settling a debt. The Internal Revenue Code, which spans over 74,000 pages, isn’t a list of punishments; it’s a series of incentives. It’s written to reward those who build, invest, and create jobs. If you aren’t actively using these incentives to structure your holdings, you’re voluntarily overpaying. Refining the questions to ask a potential tax advisor is the first step in moving from a victim of the tax code to a master of it.

The Cost of Reactive vs. Proactive Planning

Reactive filing misses time-sensitive opportunities that vanish on December 31st. For instance, failing to execute a strategic Roth conversion during a lower-income year or missing a tax-loss harvesting window can cost an investor upwards of $50,000 in immediate and future tax-free growth. This lead to “tax drag,” a silent killer of compound interest. A 2% annual tax drag on a $5 million portfolio can result in a $4.8 million loss in potential wealth over a 20-year horizon. Advanced Tax Planning is a forward-looking engineering discipline designed to optimize cash flow and maximize after-tax alpha through structural precision.

Signs You Have Outgrown Your Current Preparer

- Radio Silence: You only hear from them during the spring “crunch.” If your advisor isn’t reaching out in October or November to finalize year-end maneuvers, they aren’t acting as your strategist.

- The Ceiling of “No”: They tell you “there is nothing else we can do” to lower your bill. This usually means they’ve reached the limit of their own technical knowledge, not the limit of the law.

- Filing vs. Structuring: They focus on the mechanics of the 1040 or K-1 rather than the architecture of your estate. They treat your income as a static figure rather than a variable that can be managed.

If these signs resonate, it’s time to shift your perspective. You don’t need someone to tell you what you owed yesterday. You need an elite tactician to tell you what you can keep tomorrow. Identifying these gaps is one of the most critical questions to ask a potential tax advisor before you trust them with your legacy. It’s the difference between merely filing and truly building wealth.

5 Core Questions to Ask a Potential Tax Advisor in 2026

Stop settling for tax preparers who merely record history. If you’re earning over $500,000 annually, your tax liability isn’t just a bill; it’s a strategic variable that requires aggressive management. You need a tactician who wins the war for money and success, not a clerk who fills out forms. When interviewing, these are the critical questions to ask a potential tax advisor to ensure they can handle a high-velocity portfolio.

The 2026 tax landscape is a battlefield. With the expiration of core Tax Cuts and Jobs Act (TCJA) provisions, including the 37% top individual rate reverting to 39.6%, your strategy must be forward-looking. Ask these five core questions to identify an elite partner:

- Do you provide a written, forward-looking tax strategy or just compliance? Filing is the bare minimum. You need a 10-page “Tax Blueprint” that engineers your future, not just a summary of your past.

- How do you handle complex assets like RSUs, ISOs, and AMT exposure? Tech executives often lose 40% of their equity value to poor timing. Your advisor must understand the nuances of Section 83(i) elections and alternative minimum tax triggers.

- Can you explain your experience with multi-entity structuring? If you own a business, you shouldn’t have a single-layered entity. Ask how they use C-Corp overlays or family management companies to shift income and protect assets.

- How many clients do you serve, and what is your “white-glove” service model? Scale is the enemy of quality. If a partner manages 2,000 clients, you’re getting an intern’s attention. Demand a boutique ratio.

- How do you integrate tax planning with my broader wealth management and estate goals? Taxes don’t exist in a vacuum. A strategist must align your 1040 with your trust architecture and your low-correlation alpha investments.

Probing for Strategic Depth

Demand to see an anonymized Tax Blueprint. If an advisor’s response to a complex problem is “we follow the law,” they’re a defensive player. You want an architect who uses the law to build a fortress. Listen for proactive language. They should talk about “income shifting,” “basis step-ups,” and “harvesting losses” before you even bring them up. You can start by reviewing this questions to ask a potential tax preparer list from Forbes to cover the basics, then push for the institutional-grade insights that move the needle for high-earners.

The Exclusivity Factor

Exclusivity isn’t about ego; it’s about bandwidth. Large retail firms focus on volume, which leads to missed deductions and overlooked credits. A firm with fewer than 1,000 clients total ensures that a senior strategist, not a junior associate, reviews every K1 and 1099. Ask directly: “Who will be my primary point of contact during a mid-year strategy pivot?” If it’s not the person sitting across from you, walk away. Mastering these questions to ask a potential tax advisor will separate the administrative filers from the strategic architects who actually protect your capital.

If you’re ready to flip the script on the tax system, consider an institutional-grade strategy session to protect your legacy and keep what you’ve earned. Your wealth deserves more than a standard filing; it requires a bespoke framework designed for the 2026 shift.

Technical Deep-Dive: Questions for Sophisticated Financial Profiles

High-income earners often find themselves trapped in a tax architecture built for the average person. You don’t need a bookkeeper; you need a strategist who understands that your wealth is a complex web of equity, incentives, and multi-jurisdictional liabilities. The questions to ask a potential tax advisor must move beyond basic compliance and into the realm of financial engineering. You’re looking for a tactician who can lead your mission to protect capital and win the war for money and success.

Equity Compensation and AMT Exposure

Tech executives face a specific tax cliff where 45% of their total compensation can vanish into federal and state coffers without a precise blueprint. Ask your advisor how they model the tax impact of ISO exercises versus RSU vesting cycles. Do they have a plan for the 2026 AMT triggers? With the Tax Cuts and Jobs Act provisions set to sunset on December 31, 2025, the Alternative Minimum Tax will likely snare 3.5 million more high-earners than it does today. If they can’t run a five-year projection of your AMT exposure, they’re recording history rather than shaping it.

- Exercise Strategies: Ask if they use “sell-to-cover” or “cash-less” exercise models and how those choices impact your long-term capital gains clock.

- Concentration Risk: Inquire how they balance the tax cost of diversification against the risk of holding a single tech stock that represents 70% of your net worth.

- 83(b) Elections: Confirm their process for filing 83(b) elections within the strict 30-day window for restricted stock grants.

Multi-State and Multi-Entity Complexity

Complexity scales alongside your success. If you’re managing entities across state lines, you must know how they handle nexus and state-specific apportionment. Moving operations or residency from California to Nevada or Florida requires more than just a change of address; it requires a defensive strategy against aggressive state audits that often claw back revenue years after a move. You can explore these strategies further in our guide to Advanced Tax Planning for HNWIs. Ask how they optimize the 20% QBI deduction for your specific K1 distributions. A 2% error in entity structuring can cost a business owner $100,000 or more in unnecessary taxes over a three-year period.

The elite advisor distinguishes between reckless tax schemes and sophisticated tax engineering. Ask them to define the line between aggressive and legal optimization. A top-tier strategist cites specific tax court cases or IRS private letter rulings to support their frameworks. If their only response to a complex strategy is that the IRS might not like it, they’re a historian. You need an architect who builds a fortress around your assets using Section 831(b) for captive insurance or structured installment sales.

Institutional-Grade Investments and Alpha

Your tax advisor should understand how low-correlation alpha and institutional-grade private placements impact your 1040. Standard retail advisors often ignore the tax drag of these vehicles. Ask how they integrate your tax plan with your investment portfolio to ensure you aren’t losing 30% of your gains to inefficient distributions. They should be looking for ways to flip the script on the tax system, transforming ordinary income into favored capital gains or tax-free growth. This isn’t just about filing; it’s about engineering a legacy that survives the next decade of fiscal volatility.

Red Flags and Green Flags: Evaluating the Interview

The interview process serves as your primary filter. It separates administrative clerks from elite wealth architects. When you deploy specific questions to ask a potential tax advisor, you aren’t just looking for answers. You’re looking for a mindset. You need a partner who views tax as a controllable variable, not a fixed cost of doing business. If the conversation feels like a deposition rather than a strategic briefing, you’re in the wrong room.

For international executives and entrepreneurs, communicating these complex ideas with confidence is just as critical. Many leaders fine-tune their American accent and fluency with programs like InPronunci to ensure nothing is lost in translation during these high-stakes discussions.

Commodity pricing is the first major red flag. If an advisor charges only by the hour or per form, they’re selling their time instead of their talent. This model creates a fundamental conflict of interest. It rewards inefficiency and focuses on the past. An elite strategist understands that the most expensive bill you’ll ever pay is the tax you didn’t have to. You want a professional who leads with value, not a stopwatch. If they don’t ask about your long-term legacy or estate goals within the first thirty minutes, they’re merely historians, not architects.

Green flags are equally distinct. A sophisticated advisor leads with questions about your business structure and cash flow. They look for “tax leaks” in your current entity architecture. They also bring an institutional-grade infrastructure to the table. You shouldn’t have to coordinate between a separate CPA, an attorney, and a wealth manager. A green-flag firm provides an in-house team of 70+ professionals who collaborate on a single, unified blueprint for your success.

Understanding Fee Structures

Flat-fee or project-based billing aligns your interests with your advisor’s. This structure removes the “ticking clock” and replaces it with a focus on results. Consider the Value-Add calculation. If an elite strategist identifies a multi-entity structure that saves you $120,000 in annual tax drag, a $15,000 fee represents an 8x return on investment. Cheap tax prep is a trap. A 2023 study by the Spectrem Group found that 70% of wealthy families lose their wealth by the second generation because they lack integrated strategies. Don’t let a “cheap” bill cost you your legacy.

The Holistic Advisory Check

Does the advisor understand asset protection strategies? You need someone who talks about “flipping the script” on the tax system. They should view the financial world as a battlefield where you need a superior tactician. This requires a “War for Money and Success” mindset. They shouldn’t just help you “stay out of trouble” with the IRS. They should engineer a framework that protects your assets from litigation, inflation, and unnecessary taxation. This level of mastery is the only way to ensure you win the long game.

Ultimately, this high-stakes relationship with an advisor is about more than just technical skill; it’s about profound trust and leadership. These are the same principles that guide successful teams in any field. Keynote speaker Michael Hingson often discusses how to build this kind of effective partnership, which is just as crucial in wealth management as it is in any other high-performance environment.

When you’re evaluating the right questions to ask a potential tax advisor, pay attention to their team. Do they have in-house tax attorneys who can draft complex trust documents? Do they have wealth managers who understand low-correlation alpha? If they have to outsource these functions, your strategy will eventually crack under the pressure of poor communication. You deserve a white-glove experience that handles every granular detail of your financial architecture.

Ready to move beyond filing and start winning? Engineer your wealth architecture today.

The Neil Jesani Approach: Beyond Filing

Most traditional firms function as historians. They look at your past year, record the damage, and tell you what you owe. We’ve spent 25 years flipping that script. Our firm operates as a Strategic Architect, engineering bespoke tax blueprints that treat wealth protection as a high-stakes mission. When you evaluate the questions to ask a potential tax advisor, you shouldn’t just focus on their credentials. You need to ask if they have the structural capacity to handle complex, multi-entity puzzles that involve RSUs, ISOs, and institutional-grade wealth management.

Our “Strategic Architect” model is built on the reality that a lone CPA isn’t enough for elite clients. Your financial life has too many moving parts for a generalist. That’s why our internal team integrates 70+ professionals, including CPAs, tax attorneys, and fractional CFOs. This cross-disciplinary engine allows us to view your balance sheet through multiple lenses simultaneously. We don’t just file forms; we build frameworks. We apply 200+ years of combined heritage to ensure your tax strategy isn’t a standalone document but a living part of your legacy.

Exclusivity is a core pillar of our philosophy. While massive corporate firms chase thousands of clients to maximize volume, we deliberately serve fewer than 1,000 clients nationwide. This cap ensures every individual receives a white-glove experience. You aren’t a number in a database; you’re a partner in a high-value strategy. This limited capacity allows us to maintain a proactive advocacy stance, identifying opportunities for 30% to 50% tax savings before the fiscal year even ends.

Winning the War for Money and Success

Wealth isn’t just about what you earn; it’s about what you defend. Our brand philosophy is rooted in the idea that high-earners are often unfairly targeted by an inefficient system. We provide a proactive defense. With a strategic presence in Florida, Nevada, and California, we offer a national reach that understands the specific nuances of tax-friendly jurisdictions and high-tax tech hubs alike. From your first consultation, you’ll feel the difference of a firm that acts as your lead tactician in the war for money and success.

Your Blueprint for 2026 and Beyond

The clock is ticking on the current tax landscape. With major provisions of the 2017 Tax Cuts and Jobs Act set to sunset by 2026, the strategies that worked yesterday will fail tomorrow. You can’t afford to be reactive. We integrate institutional-grade wealth management with forward-looking tax engineering to protect your assets against upcoming legislative shifts. If you’re ready to stop being a passive participant in your tax story, it’s time to change your trajectory. Schedule your Advanced Tax Strategy Session today and let’s start building your architectural blueprint for total wealth mastery.

- Bespoke Engineering: Strategies tailored to ultra-high-net-worth complexities.

- Elite Team: Direct access to attorneys and CFOs, not just junior preparers.

- National Reach: Expert guidance across FL, NV, and CA markets.

- Future-Proofing: Specific planning for the 2026 tax law cliff.

Don’t settle for a historian when you need a strategist. The right questions to ask a potential tax advisor should lead you to a partner who is as invested in your growth as you are. We don’t just manage taxes; we optimize your entire financial existence.

Architect Your Financial Future Beyond the Filing Deadline

Stop settling for a financial historian who merely records your losses. You need a strategic architect who engineers your future wealth. By utilizing the right questions to ask a potential tax advisor, you’ll quickly separate basic compliance fillers from elite wealth protectors. Your tax strategy shouldn’t be a reactive scramble every April; it’s a year-round offensive designed to minimize tax drag and maximize your family legacy. High earners often find themselves trapped in outdated systems that prioritize the IRS over their own balance sheets.

At Neil Jesani, we maintain an intentionally limited roster of fewer than 1,000 exclusive clients to ensure every strategy receives a bespoke, white-glove touch. Our in-house team of CPAs, Tax Attorneys, and Enrolled Agents leverages 200+ years of combined heritage to build your financial blueprint. We don’t just file forms. We engineer institutional-grade frameworks that help you win the war for money and success. It’s time to stop looking backward and start building a fortress around your assets.

Secure your wealth with an elite Tax Strategy Session and take command of your financial destiny today. You’ve worked too hard to let inefficient planning erode your success.

Frequently Asked Questions

What is the difference between a tax preparer and a tax advisor?

A tax preparer focuses on historical compliance while a tax advisor engineers your financial future. Preparers spend their time looking at what happened last year to fill out forms by the April 15 deadline. In contrast, an advisor creates a 365 day strategy to minimize your tax drag. While 90% of preparers only record the past, an elite advisor builds a blueprint for your next 10 years of wealth growth.

How much should a high-net-worth individual pay for tax advisory?

High-net-worth individuals typically invest between $10,000 and $50,000 annually for bespoke tax advisory services. This isn’t a simple administrative cost; it’s a strategic investment in wealth preservation. If your annual income exceeds $500,000, a sophisticated strategy often yields a 4 to 1 return on the fees you pay. You’re paying for institutional grade expertise that prevents six figure leaks in your portfolio.

Can a tax advisor help with asset protection and estate planning?

Yes, elite advisors integrate asset protection and estate planning into a single, holistic framework to shield your legacy. They use multi-entity structuring to protect 100% of your core assets from creditors and litigation. This is one of the vital questions to ask a potential tax advisor to ensure they can manage your entire financial architecture rather than just your income tax return.

Is it worth hiring a tax advisor if I already have a bookkeeper?

Hiring an advisor is essential because bookkeepers manage the pennies while advisors protect the millions. A bookkeeper tracks $1.00 transactions to ensure your ledger balances. An advisor identifies $50,000 in missed deductions through advanced strategies like cost segregation or R&D credits. You need a bookkeeper for the data, but you need an advisor to win the war for money and success.

How often should I meet with my tax advisor?

You should meet with your advisor at least 4 times per year to adjust your strategy for market shifts and income changes. Meeting only once a year is a recipe for missed opportunities and “April surprises.” Quarterly briefings allow you to pivot your strategy every 90 days. This proactive rhythm ensures your tax blueprint stays aligned with your evolving business and investment goals.

What documents should I bring to a first meeting with a potential advisor?

Bring your last 2 years of federal and state tax returns, current K-1s, and your latest investment statements. If you’re a tech executive, include your RSU vesting schedule and ISO grant documents. Providing these 3 specific data sets allows an expert to spot structural flaws in your current plan. These documents are necessary to get real value from the questions to ask a potential tax advisor during your consultation.

Do elite tax advisors offer audit protection?

Elite advisors provide comprehensive audit representation as a core part of their white-glove service. They don’t just react to IRS notices; they engineer your filings to be audit-proof from the start. Since the IRS increased its budget by $80 billion in 2022, high-earners face a higher risk of scrutiny. A strategic advisor acts as your lead tactician, handling 100% of the communication with tax authorities.

How does a tax advisor handle RSUs and ISOs differently than a CPA?

A tax advisor proactively manages the timing of your RSU and ISO exercises to minimize AMT exposure, while a CPA often just reports the tax after it’s too late. Advisors use 83(b) elections and 10b5-1 plans to lock in long-term capital gains rates. This strategic timing can reduce your effective tax rate by 20% or more. They don’t just record the event; they architect the outcome.