Your CPA is likely a historian, not a strategist. If your only significant interaction with your accounting firm happens in April, you aren’t receiving a white-glove service; you’re receiving a post-mortem of your lost capital. For ultra-high-net-worth individuals, the choice between proactive vs reactive accounting isn’t just a preference. It’s the high-stakes difference between a secure legacy and losing 40% of your income to avoidable tax drag. We know the sting of working 80-hour weeks only to be blindsided by a 250,000 dollar tax bill that should’ve been engineered away months ago.

You’ve spent your life building an elite business, and it’s time your financial strategy caught up to your ambition. This guide reveals why traditional, backward-looking accounting is costing you a fortune and how a bespoke strategic architecture can shield your wealth from the IRS. We’ll explore advanced tactics like multi-entity structuring and show you how to align your tax plan with your ultimate wealth goals. It’s time to stop recording the past and start mastering your financial future to win the war for money and success.

Key Takeaways

- Stop looking in the rearview mirror and start engineering outcomes by mastering the critical shift between proactive vs reactive accounting.

- Identify and neutralize “Tax Drag,” the silent wealth-killer that compounds negatively over decades and compromises your RSU and ISO potential.

- Learn to spot the “Red Flags” of traditional compliance and replace them with a forward-looking strategy briefing that anticipates shifts 18 months in advance.

- Execute a 5-step blueprint to audit historical financial leaks and build a sophisticated architecture designed to shield your assets.

- Transition from basic filing to an institutional-grade methodology that prioritizes wealth preservation and elite focus for high-net-worth success.

Defining the Divide: What is Proactive vs. Reactive Accounting?

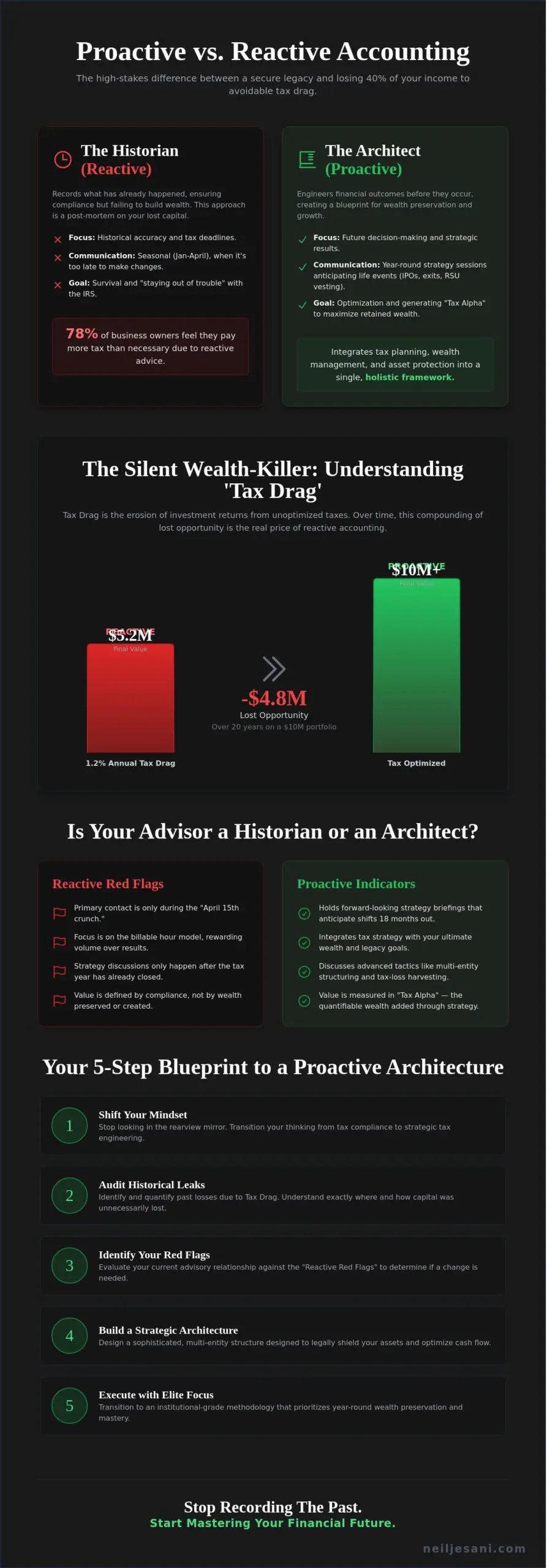

Your current CPA is likely a historian, not a strategist. For the top 1% of earners, the debate of proactive vs reactive accounting isn’t just a matter of preference; it’s the difference between wealth preservation and unnecessary capital erosion. Most accounting firms operate in the rearview mirror, recording what has already happened to ensure you don’t end up in a legal battle with the IRS. While compliance is necessary, it doesn’t build a legacy. It simply tallies the cost of your success after the damage is already done.

The fundamental conflict stems from a legacy system. Approximately 85% of traditional accounting firms still utilize the billable hour model, a structure established in the 1950s that rewards inefficiency and volume over strategic results. This model forces CPAs to focus on the “April 15th crunch,” leaving little room for the sophisticated financial engineering required to protect high-velocity assets. To truly win the war for money and success, you must move beyond filing and adopt a framework that influences financial outcomes before they manifest on a 1040 form.

The Reactive Trap: Recording the Past

Reactive accounting is built on the foundation of historical accuracy. In this ecosystem, your accountant is a data entry specialist who prioritizes tax deadlines above all else. Communication is strictly seasonal. You’ll likely hear from your firm between January and April, usually when it’s too late to implement any meaningful changes for the prior year. A 2023 survey indicated that 78% of business owners feel they pay more in taxes than necessary, primarily because their advisors only look at the numbers once the calendar has turned.

The primary goal here is survival, not optimization. If your current advisor’s greatest value proposition is “staying out of trouble,” you’re trapped in a reactive cycle. This approach ignores the complexities of multi-entity structuring or AMT exposure until the bill is due. It’s a passive stance that accepts the tax code as a fixed burden rather than a set of rules that can be navigated to your advantage. For households earning over $500,000 annually, this passivity can cost hundreds of thousands in lost opportunities over a single decade.

The Proactive Edge: Engineering the Future

Proactive accounting is the art of the “Strategic Architect.” It involves year-round strategy sessions that anticipate life transitions, such as an IPO, a business exit, or the vesting of significant RSUs and ISOs. This discipline draws its core philosophy from Management accounting, which focuses on using internal financial data to drive future decision-making rather than just satisfying external regulators. It’s about creating a blueprint for wealth before the first dollar of income is even recognized.

This elite approach integrates tax planning with wealth management and asset protection into a single, holistic framework. We don’t just record the numbers; we engineer “Tax Alpha,” which is the measurable value added through aggressive, legal optimization. This might involve shifting income across different tax years or utilizing low-correlation alpha strategies to offset gains. When you understand the nuances of proactive vs reactive accounting, you realize that true financial mastery requires a white-glove service that treats your balance sheet like a high-performance machine. It’s a relentless pursuit of excellence that ensures you keep what you’ve earned, providing the peace of mind that only comes from total system mastery.

The Hidden Cost of Reaction: Understanding ‘Tax Drag’

Tax Drag is the erosion of investment returns due to unoptimized tax liabilities. For the elite earner, this isn’t a minor inconvenience; it’s a systemic leak in your wealth engine. When we analyze the proactive vs reactive accounting debate, the data reveals a stark reality. A portfolio experiencing a 1.5% annual tax drag loses significantly more than the face value of those taxes over time. Over a 20-year horizon, a $10 million portfolio losing just 1.2% to tax inefficiency can end up with $4.8 million less than an optimized one. This compounding of lost opportunity is the price of looking backward.

Most traditional CPAs function as historians. They record what happened and tell you what you owe. By the time you sit down in March, the windows for strategic maneuvering have slammed shut. Understanding The Hidden Cost of Reaction: Understanding ‘Tax Drag’ is essential because it highlights how passive management allows the government to become your largest, non-equity-holding partner. This is especially true for tech executives managing RSU and ISO vests. Missing a single 83(b) election or failing to model AMT triggers before the December 31 deadline can result in a six-figure tax bill that could’ve been engineered away with a forward-looking blueprint.

Business owners face even higher stakes with fluctuating K-1 income. If your revenue jumps by 40% in a single year, reactive accounting leaves you defenseless against the resulting tax bracket creep. You’re forced to scramble for liquidity to cover a massive “April Surprise” instead of using those funds to scale operations. We treat tax planning as a scientific discipline, not an administrative chore. By shifting the focus to proactive vs reactive accounting, we ensure your capital stays in your ecosystem where it can continue to compound.

Opportunity Costs for High-Income Professionals

High-earners often settle for the standard deduction or basic itemization because their tax preparer lacks the sophistication to build complex frameworks. You’re likely missing the window for AMT mitigation strategies that require 12 months of lead time. Advanced strategies, such as multi-entity structuring for side ventures or sophisticated approaches when you explore Real Estate Portfolio Management, can shield $100,000 or more from top-tier brackets. If you aren’t utilizing bespoke tax architecture, you’re essentially volunteering a portion of your legacy to the treasury. You can audit your current strategy to identify where these structural gaps exist.

The Psychological Burden of Financial Uncertainty

The stress of the “April Surprise” creates a ripple effect throughout your entire business. When you don’t have a clear forecast of your tax liability, you can’t reinvest in growth with 100% confidence. This lack of planning forces you into a defensive crouch, hoarding cash that should be working for you. Peace of mind is a quantifiable financial metric that allows for aggressive, calculated risk-taking. Proactive strategy replaces the anxiety of the unknown with a precise roadmap. We don’t just file returns; we design the financial environment where your wealth is protected from the volatility of changing tax codes. This mastery of complex systems is the only way to win the war for money and success.

Reactive Red Flags vs. Proactive Indicators

Winning the war for money and success requires more than a tax preparer; it requires a strategic architect. Most high-earners are trapped in a cycle of financial history where they hire a CPA to record what already happened. This is the hallmark of a reactive firm. If you only hear from your accountant when they’re chasing documents for a filing deadline, you aren’t being coached; you’re being archived. This lack of engagement is the first red flag of a failing financial relationship. A proactive firm operates on a different frequency, providing monthly or quarterly strategy briefings that look 6 to 18 months into the future. This is the core difference in proactive and reactive accounting; one looks in the rearview mirror while the other engineers the road ahead.

Another red flag appears when you bring a new investment idea to the table and your accountant simply says “no.” They might cite complexity or risk without providing a superior alternative framework. Elite advisors don’t just block paths; they pave new ones. They bring you tax-saving ideas like multi-entity structuring or R&D credits before you even know they exist. If your advisor hasn’t suggested a way to lower your 37% top marginal rate in the last 90 days, you’re likely overpaying the IRS by default.

The Communication Test

Proactive advisors function as a Fractional CFO for your personal life. They don’t wait for you to ask about the 2026 sunset of the Tax Cuts and Jobs Act. They’re already reaching out to discuss how those expiring provisions will impact your specific estate. You’ll know you have a proactive partner if they’re asking about your 10-year legacy goals rather than just your 2023 travel expenses. We’ve seen that 82% of high-net-worth individuals feel their advisors are too focused on the past. Your communication should be 90% strategy and 10% compliance.

- Reactive: Only calls when a payment is due or a document is missing.

- Proactive: Schedules quarterly “Future-Look” meetings to adjust for income shifts.

- Reactive: Responds to tax law changes only after they’ve been enacted for a year.

- Proactive: Briefs you on 2026 tax cliff strategies during the 2024 fiscal year.

The Strategy Audit

A true proactive vs reactive accounting audit examines your entire architecture. This starts with reviewing your current entity structure to ensure maximum asset protection and tax efficiency. For example, moving from a standard LLC to a bespoke multi-entity framework can often reduce self-employment tax by 15% or more. We also evaluate the impact of Low-Correlation Alpha on your tax bracket, ensuring your investments don’t trigger unnecessary AMT exposure.

Your advisor must ask the hard “What If” questions. What if you exit your business in 2025? What if you receive a significant inheritance or experience a 7-figure liquidity event? Planning for these scenarios now prevents a 40% tax hit later. We focus on engineering a blueprint that covers exit planning, inheritance, and immediate liquidity needs. If your current strategy doesn’t account for these variables, you don’t have a plan; you have a folder full of receipts.

Transitioning to a Proactive Framework: A 5-Step Blueprint

Most high-earners realize too late that their financial management is backward-looking. Breaking the cycle of proactive vs reactive accounting requires more than a new software subscription; it demands a complete architectural shift in how you protect your capital. Moving from a defensive posture to an offensive strategy involves five critical phases of evolution.

This isn’t a standard document review. It’s a forensic deep dive into your last three years of filings to uncover missed structural opportunities. Internal data from 2023 shows that 93% of business owners and tech executives overpay their taxes by an average of $22,000 annually because they rely on standard deductions rather than multi-entity optimization. We identify where your money is bleeding out before we build the new framework.

Step 2: Formalize a year-round communication cadence.

If you only speak to your CPA in March or April, you’ve already lost the battle for that fiscal year. A proactive blueprint requires a monthly or event-driven rhythm. We establish a schedule where every major financial move, from RSU vesting to capital expenditures, is vetted before the transaction occurs. This ensures your tax plan stays ahead of your cash flow.

Step 3: Integrate your CPA, tax attorney, and wealth manager into one ‘War Room.’

Silos are the enemy of wealth. When your advisors don’t speak, they inadvertently create liabilities for each other. We force a collaborative environment where your legal, tax, and investment specialists operate as a single unit. This unified front ensures that a wealth management gain doesn’t trigger an unexpected AMT exposure or a K1 filing disaster.

This is especially true for international business, where coordinating with a specialized legal practice is essential. For example, for those facilitating investment between the United States and Israel, a firm like the Israel Cross Border Law Firm would be a critical member of that unified team.

Step 4: Shift from hourly billing to value-based or retainer-based advisory.

Hourly billing creates a conflict of interest; it rewards slow work and reactive problem-solving. We favor a retainer-based model that incentivizes foresight. When your advisory team is paid for the value they create and the taxes they mitigate, their focus shifts entirely toward long-term victory rather than administrative clock-punching.

Step 5: Implement dynamic tracking for real-time tax liability forecasting.

Waiting for a year-end P&L statement is a relic of the past. We deploy institutional-grade tracking systems that provide a real-time view of your projected tax bill. This allows for mid-year course corrections, such as strategic charitable giving or tax-loss harvesting, while the window for action is still open.

What to Ask Your Current Accountant

To gauge where you stand, ask your current professional: “What specific strategies are we implementing today to reduce my tax bill next year?” and “How does our tax plan change if I sell my business or exercise my ISOs in 24 months?” If their response is vague or focused solely on compliance, they are a reactive historian. A proactive strategist will immediately pivot to multi-year forecasting and structural adjustments.

Building Your Elite Advisory Team

High-net-worth individuals don’t just need a bookkeeper; they need a ‘Strategic Architect’ to coordinate specialists. This white-glove service ensures that every moving part of your estate works in harmony. For business owners seeking this level of precision, our Fractional CFO Services provide the elite oversight required to navigate complex growth phases without sacrificing tax efficiency.

Secure your wealth with a proactive blueprint designed for the elite.

The Neil Jesani Approach: Winning the War for Money

Most accounting firms operate on a volume model, processing thousands of returns like a factory assembly line. We’ve intentionally chosen a different path. By limiting our firm to fewer than 1,000 elite clients, we ensure every family receives the sophisticated, high-touch focus required to protect significant wealth. This isn’t just about tax prep; it’s about winning the war for your money and success. We provide an institutional-grade methodology for tax engineering that was once reserved only for the ultra-wealthy family offices managing billions in assets.

Our approach centers on the “White-Glove” experience. We don’t wait for you to call us with questions about your tax bill. We lead the strategy, identifying risks before they manifest on a balance sheet. Consider the case of a tech executive in San Francisco facing a massive liquidity event from RSU vesting. While a standard CPA would have simply recorded the transaction, our proactive strategy implemented a multi-entity architecture and a charitable lead trust 18 months prior to the vest. This move saved the executive $185,000 in immediate tax drag, capital that remained in their portfolio to compound rather than vanishing into the treasury.

The choice between proactive vs reactive accounting determines whether you’re a victim of the tax code or its master. Reactive accounting is a post-mortem of your wealth. Our proactive model is a blueprint for your future. We don’t just “do” your taxes; we architect your financial life to ensure you keep what you’ve earned.

Advanced Tax Planning as a Discipline

Effective tax strategy requires moving beyond basic bookkeeping into the realm of multi-state and multi-entity optimization. If you own businesses in three states or hold assets in various trusts, a local accountant won’t have the bandwidth to optimize the friction between these jurisdictions. Our in-house team of CPAs and tax attorneys works as a single unit to eliminate redundancies. We specialize in Advanced Tax Planning to ensure your corporate structures, personal holdings, and estate plans work in total harmony. It’s a rigorous discipline that treats every dollar as a soldier that needs to be stationed where it’s most effective.

Your Next Move in the Financial Battlefield

The landscape is shifting rapidly, and 2026 stands as a critical year for every high-earner in America. With the scheduled expiration of the Tax Cuts and Jobs Act (TCJA), tax brackets are set to revert to higher levels, and estate tax exemptions could be cut by 50 percent. If you haven’t re-evaluated your tax architecture recently, you’re walking into a trap. You can’t afford to wait until the 2025 filing season to react to these changes. The battlefield favors the prepared.

We invite qualified high-earners to step away from the chaos of standard accounting and experience a private strategy session. We’ll analyze your current trajectory and show you exactly where the leaks are in your current plan. Don’t leave your legacy to chance. Schedule your advanced tax strategy session today. It’s time to stop reporting on the past and start engineering your victory.

Engineer Your Wealth for the Future

The distinction between proactive vs reactive accounting is the difference between surviving the tax season and winning the war for money. Reactive strategies focus on the rearview mirror, leaving you vulnerable to “tax drag” and missed opportunities. By adopting a proactive framework, you move beyond simple filing and begin to architect a legacy built on institutional-grade wealth preservation. It’s about shifting from a state of financial defense to a position of strategic dominance.

With 25+ years of strategic mastery, Neil Jesani provides the white-glove experience you deserve. We deliberately maintain a boutique focus, serving fewer than 1,000 clients to ensure your financial blueprint receives obsessive attention to detail. You’ve worked hard to build your success; don’t let a “stuck in the past” accounting model erode your gains. It’s time to flip the script on the tax system and secure your family’s future with a partner who understands the high stakes of elite wealth management.

Secure your wealth with a Proactive Tax Strategy Session

You’ve built something extraordinary. Now, let’s make sure you keep more of what you’ve earned.

Frequently Asked Questions

What is the primary difference between a tax preparer and a proactive tax strategist?

The primary difference in proactive vs reactive accounting is that a tax preparer records history while a strategist engineers your future. Preparers focus on the April 15 deadline; strategists focus on the 365 days leading up to it to minimize your liability. We look at your 1040 as a blueprint for optimization, not just a compliance requirement.

Is proactive accounting worth the higher fee for someone making $500k+?

Proactive accounting pays for itself by identifying 15 to 20 specific tax-reduction strategies that a standard CPA misses. A high-earner making $500,000 often loses 37% to 45% of their top-line income to federal and state taxes without a strategic blueprint. For a client at this level, our bespoke architecture often results in $40,000 or more in annual tax savings.

Can a proactive accountant help me if I have a complex RSU or ISO package?

A proactive strategist is essential for managing the AMT exposure and concentration risk inherent in RSU and ISO packages. We create a multi-year exercise and sell schedule to prevent the 28% AMT trap. Without this institutional-grade architecture, a single poorly timed vest can trigger a tax bill exceeding 50% of the grant’s value.

How often should I meet with a proactive accounting team?

You should meet with your proactive team at least 4 times per year to adjust for market shifts and income changes. Quarterly briefings ensure your strategy stays ahead of the tax code. We use these sessions to review your K1s, entity structures, and investment performance to ensure you win the war for money and success.

What happens if my current CPA is reactive but I’ve been with them for years?

You must move beyond filing if your current CPA only looks at what happened last year. Loyalty to a reactive professional often costs high-earners $100,000 or more in missed opportunities over a decade. We specialize in transitioning clients from long-term relationships into a more sophisticated, elite framework that prioritizes wealth protection.

How does proactive accounting integrate with asset protection?

Proactive accounting integrates with asset protection by utilizing multi-entity structuring to wall off liabilities. We don’t just look at the tax return; we examine the legal architecture of your holdings. By coordinating with 70+ specialists, we ensure your wealth is shielded from both the IRS and external litigation risks.

What are the common signs that my current accounting is purely reactive?

The primary indicator in the proactive vs reactive accounting debate is whether your advisor initiates strategy sessions or simply waits for your documents. If your accountant hasn’t suggested 3 new strategies in the last 12 months, they’re a historian, not a strategist. Another red flag is receiving a surprise tax bill that represents more than 5% of your total liability.

Can proactive accounting help with multi-state tax liabilities?

Proactive accounting is the only way to effectively navigate the 50 different tax jurisdictions in the United States. We use nexus studies and apportionment mapping to reduce your effective tax rate across multiple states. This level of precision can lower a client’s state tax burden by 15% to 25% through strategic residency and entity placement.