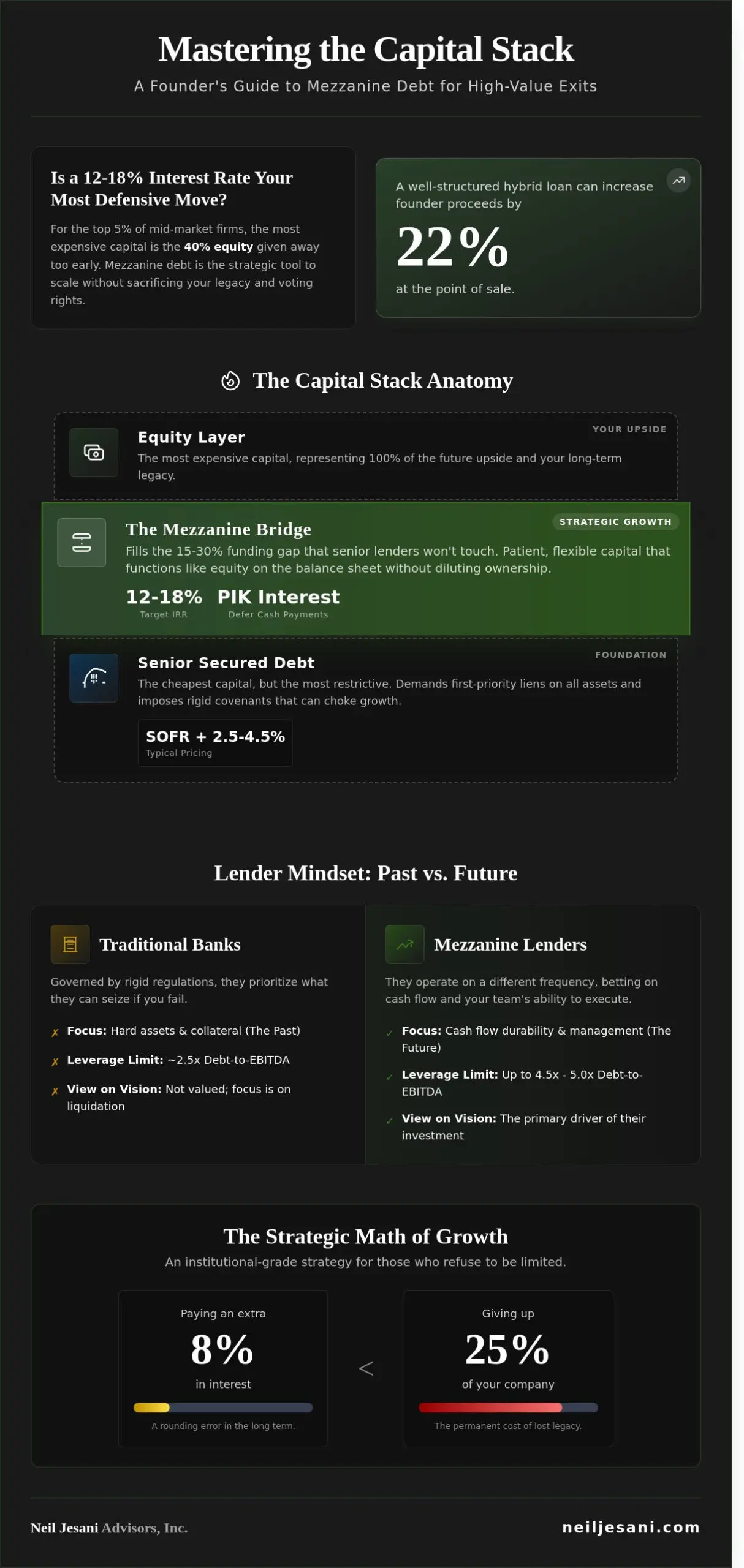

What if the 12% to 18% interest rate on your next capital raise was actually the most defensive move you could make for your legacy? For many elite founders, the fear of mezzanine debt stems from a misunderstanding of its architecture; yet, it remains the preferred tool for the top 5% of mid-market firms looking to scale without 40% equity dilution. You’re right to be wary of complex PIK interest structures and the perceived high cost compared to traditional senior bank loans. In the war for market dominance, the most expensive money is almost always the equity you give away too early.

I promise to help you master these complexities so you can engineer a high-value exit while keeping your voting rights intact. We’ve optimized capital stacks for over 950 high-net-worth clients, and our internal benchmarks show that a well-structured hybrid loan can increase founder proceeds by 22% at the point of sale. This guide breaks down exactly where this capital fits in your stack, evaluates the real ROI of hybrid financing, and provides a blueprint to protect your equity from aggressive lenders.

Key Takeaways

- Master the architecture of your capital stack to bridge funding gaps and fuel expansion without sacrificing your hard-earned equity.

- Deconstruct the sophisticated mechanics of mezzanine debt, including PIK interest and equity kickers, to negotiate bespoke terms that favor elite business owners.

- Distinguish between predatory borrowing and tactical growth by applying a rigorous strategic checklist before deploying high-leverage capital.

- Align your financing with institutional-grade exit planning methodologies to engineer a high-value transition that preserves your wealth and legacy.

- Integrate proactive tax planning into your debt repayment strategy to ensure you are building a future-focused blueprint rather than just managing the past.

Understanding Mezzanine Debt: The Bridge in Your Capital Architecture

Most high-performing business owners view financing as a binary choice between a restrictive bank loan and surrendering a massive piece of their legacy to equity partners. It’s a false dichotomy that kills momentum. As a Strategic Architect, you must look at your balance sheet as a high-stakes battlefield where every dollar of capital has a specific rank and a distinct mission. Mezzanine debt serves as the elite specialized unit in this hierarchy. It’s a hybrid instrument that blends the characteristics of debt and equity; it’s designed specifically to fill the funding void when senior lenders reach their regulatory or risk-appetite limits.

This capital layer doesn’t just provide liquidity; it provides tactical flexibility. Because it’s “subordinated” to senior debt, it occupies a unique space in the hierarchy of claims. In a liquidation event, the mezzanine lender waits until the senior bank is paid in full before receiving a dime. This junior status creates a higher risk profile for the lender, which is why they demand higher returns. However, for the business owner, this subordination is a powerful lever. It allows you to access capital that functions like equity for your balance sheet strength but doesn’t require you to hand over the keys to your boardroom. This Mezzanine capital overview confirms its role as a critical bridge for mid-market companies seeking to execute 2024 expansion plans without massive dilution.

The Capital Stack Anatomy

To win the war for money and success, you must master the architecture of your capital stack. Think of it as a three-tiered blueprint for growth:

- Senior Secured Debt: This is your foundation. In the current 2024 credit environment, this is the cheapest capital available, typically priced at SOFR plus 250 to 450 basis points. Banks demand first-priority liens on all assets and impose rigid covenants that can choke a growing firm.

- Mezzanine Layer: This fills the 15% to 30% gap that senior lenders won’t touch. It’s patient capital. It often features “PIK” (Payment-in-Kind) interest options, allowing you to defer cash payments and reinvest that capital into immediate operations.

- Equity Layer: This is the most expensive capital you’ll ever “buy.” While it carries no interest, it represents 100% of the future upside. Using mezzanine debt to replace a portion of this layer preserves your ownership and protects your long-term legacy.

Why Traditional Banks Say No

Commercial banks are governed by rigid regulatory frameworks that prioritize asset coverage above all else. If your business doesn’t have a surplus of machinery, real estate, or high-quality receivables to pledge as collateral, the bank typically stops lending once you hit a 2.5x Debt-to-EBITDA ratio. They’re looking at the past; they’re looking at what they can seize if you fail. They don’t value your vision or your projected growth trajectory.

Mezzanine lenders operate on a different frequency. They ignore hard assets and focus almost exclusively on the durability of your cash flow and the strength of your management team. They’ll often extend leverage to 4.5x or even 5.0x EBITDA. You’ll pay a higher coupon, often between 12% and 18%, but the math is clear. Paying an extra 8% in interest is a rounding error compared to the cost of giving up 25% of a company that’s doubling in value every three years. It’s an institutional-grade strategy for those who refuse to be limited by the conservative nature of traditional retail banking.

The Mechanics of Hybrid Financing: PIK Interest and Equity Kickers

Standard bank loans are off-the-rack products designed for the average borrower. Mezzanine debt is a tailored Savile Row suit engineered for the elite business owner. It represents a sophisticated hybrid of senior debt and equity; it’s an institutional-grade instrument that requires a strategic architect to navigate. We don’t just look at the interest rate. We deconstruct the entire 50-page credit agreement to ensure the architecture of the deal supports your legacy rather than eroding it. These terms are bespoke and highly negotiable for those who understand the leverage they hold in the private credit markets.

Sophisticated lenders view these deals through the lens of a “total return” profile. In 2024, most mezzanine funds target an internal rate of return (IRR) between 12% and 18%. Achieving this yield involves a complex blend of cash interest, deferred interest, and equity upside. As your advocates, we decipher these layers to reveal the true cost of capital. You aren’t just borrowing money; you’re entering a high-stakes partnership where every clause is a tactical move in the war for money and success.

Payment-in-Kind (PIK) Interest Explained

PIK interest is a hallmark of the mezzanine world. Instead of forcing you to deplete your monthly cash reserves, a portion of the interest is “paid in kind” by adding it to the principal balance. For a company scaling at 25% year-over-year, this is a vital liquidity tool. It allows you to reinvest every available dollar into R&D or market expansion. However, you must be wary of the snowball effect. A $10 million loan with a 4% PIK component will grow to over $12.1 million in principal after five years through the power of compounding. We help you model these outcomes to ensure the balance sheet doesn’t become a trap when it’s time to exit or refinance.

Warrants and Equity Kickers

The “kicker” is how the lender participates in your success. Lenders typically request warrants to purchase 1% to 5% of your company’s equity at a nominal price. This isn’t just a fee; it’s a claim on your future. Calculating the real cost of this dilution is essential. If your enterprise value jumps from $50 million to $150 million, a 3% warrant costs you $4.5 million in realized wealth. This is often significantly more expensive than a traditional 8% bank loan.

We focus on protective strategies to maintain founder control. This includes negotiating “caps” on warrant appreciation or implementing “put” options that allow you to buy back the warrants at a predetermined formula. Protecting your equity requires more than just a lawyer; it requires a forward-looking wealth strategy that anticipates your company’s peak valuation. Our role is to ensure that when you win the war for success, you keep the spoils.

- Negotiate the Strike Price: Push for a higher valuation at the time of issuance to minimize the “spread” the lender captures.

- Limit the Scope: Ensure warrants apply only to a specific subsidiary or entity rather than the entire holding company.

- Expiration Dates: Set tight windows for exercise to prevent the lender from riding your growth indefinitely.

The institutional-grade nature of these instruments means they’re built to favor the lender by default. You need a proactive tactician to flip the script. By engineering the PIK and warrant structures correctly, you transform a potentially dangerous debt load into a powerful engine for exponential growth.

Tool for Growth or Expensive Trap? Addressing the Mid-Market Dilemma

Critics often label mezzanine debt as predatory or usurious. They point to interest rates that typically hover between 12% and 20% as evidence of a trap. This perspective is narrow and lacks strategic depth. As a strategic architect, I view capital not by its price tag, but by its return on investment (ROI). If you use high-cost capital to plug a leaking bucket, you’re inviting disaster. If you use it to build a bridge to a $100 million exit, you’re engineering a masterpiece. You must distinguish between tactical leverage and desperate borrowing. Desperation seeks a lifeline; strategy seeks a catalyst.

The math determines the outcome. Consider a business owner earning $5 million in EBITDA. They find an acquisition target for $10 million that adds $2.5 million in immediate EBITDA. If senior lenders only provide $6 million, the owner faces a $4 million gap. Giving up 20% of the company to an equity partner might cost $20 million in future exit value. Using a mezzanine layer at 15% interest costs $600,000 annually. The choice is clear. You pay a premium for the capital to protect the equity. You’re winning the war for money by keeping the lion’s share of the upside.

When Mezzanine Debt is a Tool

Strategic growth requires aggressive moves. In the Q4 2023 credit cycle, 62% of mid-market acquisitions utilized subordinated debt to bridge valuation gaps. It’s a tool when funding a transformative acquisition that pushes your EBITDA from a 4x multiple to a 7x “platform” multiple. It works for shareholder buyouts where you need to remove a 25% partner without diluting your own 75% stake. Finally, it serves as an elite bridge for companies 18 months away from an IPO, providing the liquidity needed to scale operations without a down-round equity raise.

When Mezzanine Debt is a Trap

The trap snaps shut when the blueprint is flawed. Using mezzanine debt to cover operational “burn” or negative cash flow is a death spiral. It’s a trap when your total leverage ratio exceeds 4.5x EBITDA, potentially triggering a default on your senior debt covenants, which often require a 1.25x Debt Service Coverage Ratio (DSCR). If you don’t have a documented 24 to 36 month exit strategy to refinance or sell, you’re not borrowing; you’re gambling with your legacy. Without a clear path to liquidity, the compounding interest will eventually consume your equity cushion.

We must also address the “Tax Drag” on high-interest structures. While interest payments are deductible against your 37% top federal tax bracket, the cash flow drain is real. This drag occurs when the cost of your debt exceeds the growth rate of your enterprise value. If your business grows at 9% but your debt costs 16%, you’re effectively liquidating your company’s value to pay the lender. We engineer strategies that go beyond filing to ensure your capital structure doesn’t become a weight. You need a framework that balances the tax shield benefits against the preservation of operational cash flow. Stop thinking like a borrower. Start thinking like an architect of wealth.

Strategic Evaluation: When to Deploy Mezzanine Debt Before an Exit

Deploying mezzanine debt isn’t a casual financial decision. It’s a high-stakes maneuver for owners who refuse to settle for mediocre exit multiples. According to the Exit Planning Institute’s methodology, value acceleration requires a relentless focus on the “Four Cs”: Capital, Category, Clout, and Character. Before you sign a term sheet, you must determine if this capital will act as a propellant or a weight during your final 24 to 36 months of ownership. You’re not just borrowing money; you’re engineering a liquidity event.

Evaluate your readiness with this strategic checklist:

- Does your trailing twelve-month (TTM) EBITDA exceed $3 million with a clear path to $10 million?

- Is your projected Return on Invested Capital (ROIC) at least 25% higher than the cost of debt?

- Have you completed a Mastering Your Exit: Business Valuation and Planning assessment to benchmark your current standing?

- Can your current cash flow support a 1.25x Debt Service Coverage Ratio (DSCR) even in a 15% market downturn?

Strategic buyers don’t just look at your top line. They scrutinize how mezzanine debt has been utilized to capture market share or integrate vertical efficiencies. If you use this capital to fund a strategic acquisition that adds 300 basis points to your margin, you’ve won the tactical game. If you use it to cover operational inefficiencies, you’ve built a trap. At the point of sale, buyers calculate Enterprise Value then subtract interest-bearing debt. Your mission is to ensure the EBITDA growth fueled by the debt far outweighs the liability on the balance sheet at a 6x to 10x multiple.

Preparing the Financial Blueprint

Your EBITDA growth must aggressively outpace the 12% to 18% all-in cost of mezzanine capital to justify the risk. This is where an elite Fractional CFO becomes your most valuable asset. They don’t just report numbers; they architect the cash flow model to ensure debt service never chokes your R&D or sales engine. Strategic buyers typically hunt for a debt-to-equity ratio below 3:1. Pushing beyond this requires a bulletproof justification rooted in recurring revenue or proprietary IP that guarantees future cash flows.

Managing the Covenants

Mezzanine agreements are riddled with financial landmines known as covenants. The most common is the leverage ratio, which often restricts you from taking on additional senior debt. A “white-glove” monitoring approach is essential because a single quarter of underperformance can trigger a technical default. This doesn’t just cost fees; it creates a “hair on the deal” that can stall your exit timeline by 9 months or scare off institutional-grade buyers. Precision in compliance is your primary shield in the war for money and success.

Engineering Your Exit: Holistic Strategy Beyond the Debt

Most financial professionals operate in the rearview mirror. They focus on compliance, filing forms, and documenting what already happened. At Neil Jesani Advisors, Inc., we reject that passive model. We act as strategic architects for your future. While mezzanine debt provides the fuel for your current expansion, the real challenge lies in the endgame. You aren’t just looking for a loan; you’re looking for a bridge to a massive liquidity event. If you don’t engineer that bridge with precision, you’ll find that the “growth” you achieved was merely a transfer of wealth from your pockets to the government and your lenders.

Tax-Optimized Debt Structuring

The internal revenue code is a battlefield. Under Section 163(j), interest expense deductions are often capped at 30% of your adjusted taxable income. If your mezzanine debt carries a coupon rate between 12% and 15%, an unoptimized structure leads to a massive tax drag that erodes your internal rate of return. We go beyond simple filing. We analyze the interplay between your debt service and your multi-entity structure to maximize every cent of deductibility. When lenders exercise their warrants, it often triggers a taxable event that catches owners off guard. We blueprint the exit to ensure these conversions are handled through tax-efficient vehicles, preventing a 37% federal tax hit on your equity gains.

The White-Glove Wealth Preservation

High leverage brings high stakes. Business owners operating with institutional-grade debt need more than a standard brokerage account. They need a fortress. We implement advanced asset protection strategies that wall off your personal holdings from the operational risks of a leveraged company. As you transition from business equity to personal liquidity, we move your capital into low-correlation alpha and bespoke investment tiers usually reserved for the top 1% of earners. This isn’t just about saving money; it’s about transforming a successful business exit into a permanent family legacy. You’ve spent years building your empire. We ensure you actually keep it.

- Strategic Architecture: We design the framework for your exit years before the first “for sale” sign is ever considered.

- Institutional-Grade Solutions: Access the same sophisticated wealth tools used by tech executives and elite founders.

- Fiduciary Advocacy: We don’t answer to shareholders; we answer to you, ensuring your capital structure serves your long-term vision.

Success in the world of high-finance isn’t a matter of luck. It’s a matter of superior tactics. You can’t win the war for money and success by following the same outdated advice that middle-market firms provide. You need a partner who understands that every dollar saved in taxes and every basis point gained in debt structuring is a victory for your family’s future. It’s time to stop reacting to your balance sheet and start engineering it for maximum impact. The difference between a trap and a tool is the hand that wields it.

Engineer Your Capital Architecture for a Final Victory

Wealth preservation isn’t an accident. It’s the calculated result of superior engineering and proactive strategy. You’ve seen how mezzanine debt serves as a high-octane fuel for mid-market growth, yet it carries structural risks like PIK interest and equity kickers that can erode your hard-earned legacy. Success requires looking beyond the immediate capital infusion to the final exit. You don’t just need a loan; you need a blueprint that protects your equity while optimizing your tax position. Our elite team of 70+ CPAs and tax attorneys specializes in this level of precision. We provide a bespoke, white-glove experience for fewer than 1000 clients. We leverage 25+ years of heritage to ensure you win the war for money and success. Don’t leave your exit to chance or allow complex debt structures to dilute your life’s work. It’s time to move beyond simple filing and start mastering your financial future. You’ve built something extraordinary, and you deserve a strategy that’s equally exceptional.

Request Your Bespoke Tax and Exit Strategy Session

Frequently Asked Questions

What is the typical interest rate for mezzanine debt in 2026?

Expect mezzanine debt interest rates to range between 12% and 18% in 2026. This pricing reflects a 400 to 600 basis point premium over the Secured Overnight Financing Rate (SOFR). We engineer these structures to include a combination of cash interest and Payment-in-Kind (PIK) interest; which preserves your immediate liquidity while fueling aggressive expansion. It’s a high-stakes tool for those ready to win the war for money and success.

How does mezzanine debt differ from a traditional bank loan?

Mezzanine debt sits below senior bank debt in the capital stack and carries no requirement for hard collateral like real estate or equipment. While a traditional bank loan demands a 1.25x debt service coverage ratio and physical assets—a domain where specialists like Icon Capital LLC operate—mezzanine lenders focus on your EBITDA and enterprise value. It’s a bespoke solution for high-growth firms that have exhausted their senior borrowing capacity but refuse to slow down their momentum.

Can mezzanine debt be used for a management buyout (MBO)?

Mezzanine debt is a cornerstone of the MBO framework; typically providing 20% to 40% of the total purchase price. It bridges the critical gap between the management team’s equity contribution and the senior bank loan. This strategy allows executives to acquire companies with less personal capital. We’ve seen this blueprint empower leadership teams to transition from employees to owners without surrendering total control to outside private equity firms.

Is mezzanine debt considered “dilutive” to my ownership?

Mezzanine debt is typically “lightly dilutive” because most agreements include equity warrants representing 1% to 5% of your company’s ownership. This is the calculated price for accessing flexible, non-amortizing capital that banks won’t provide. Unlike a pure equity raise where you might lose 20% of your board seats; this structure keeps you in the driver’s seat. It’s a strategic trade-off designed to protect your long-term legacy.

What happens to mezzanine debt if the company is sold?

The mezzanine lender is paid immediately after the senior secured creditors once a sale closes. Most agreements include a “make-whole” provision or a 1% to 3% prepayment penalty if the debt is retired before a specific 3-year or 5-year window. You must account for these exit costs in your initial financial architecture. Ensuring your payoff schedule aligns with your exit strategy is critical for a white-glove transition of wealth.

How much mezzanine debt can my business realistically afford?

Most businesses can realistically afford total debt levels between 3.5x and 4.5x their annual EBITDA. If your senior bank loan covers 2.0x; you have room for roughly 1.5x to 2.5x in additional mezzanine financing. We analyze your free cash flow to ensure you maintain at least a 1.1x fixed charge coverage ratio. Over-leveraging is a trap; proper engineering ensures your debt remains a tool for growth rather than a weight.

Do I need a Fractional CFO to manage mezzanine financing?

You need a Fractional CFO or a high-level strategist to manage the rigorous monthly reporting and covenant compliance required by these lenders. Institutional-grade lenders expect sophisticated financial statements every 30 days without exception. Without a dedicated expert to monitor your leverage ratios and PIK accruals; you risk technical default. Our elite clients use these specialists to flip the script on complex financing and maintain operational peace of mind.