What if the very success you’ve spent 25 years building has actually turned you into a high-visibility target for the next predatory lawsuit? If you’re a tech executive or business owner, you already know that the legal landscape is a battlefield where the unprepared lose their legacy. You’re likely searching for how to protect your assets because you realize that traditional wealth management is built for the past, not for the high-stakes reality of modern litigation.

It’s frustrating to watch 40% to 50% of your hard-earned income disappear into tax drag while wondering if your current trusts and LLCs are actually bulletproof. We agree that you deserve a white-glove strategy that goes beyond filing and enters the realm of true financial architecture. This guide reveals the elite framework used to shield wealth from creditors and integrate sophisticated tax planning into a single, cohesive blueprint. You’ll discover how to deploy multi-entity structuring and institutional-grade legal shields to win the war for money and success.

Key Takeaways

- Identify why high-earners are prime targets and how to engineer a proactive legal framework that shields your wealth from predatory third-party claims.

- Move beyond basic liability insurance by implementing a sophisticated hierarchy of defense that utilizes strategic titling to eliminate single points of failure.

- Deploy institutional-grade entity structuring, including LLCs and Trusts, to create a robust “charging order” shield around your most valuable holdings.

- Follow a definitive 5-step blueprint on how to protect your assets, beginning with a comprehensive stress test of your current financial architecture.

- Flip the script on the tax system by integrating advanced tax planning as your primary defense against wealth erosion and unnecessary tax drag.

What is Asset Protection? Engineering Your Financial Fortress

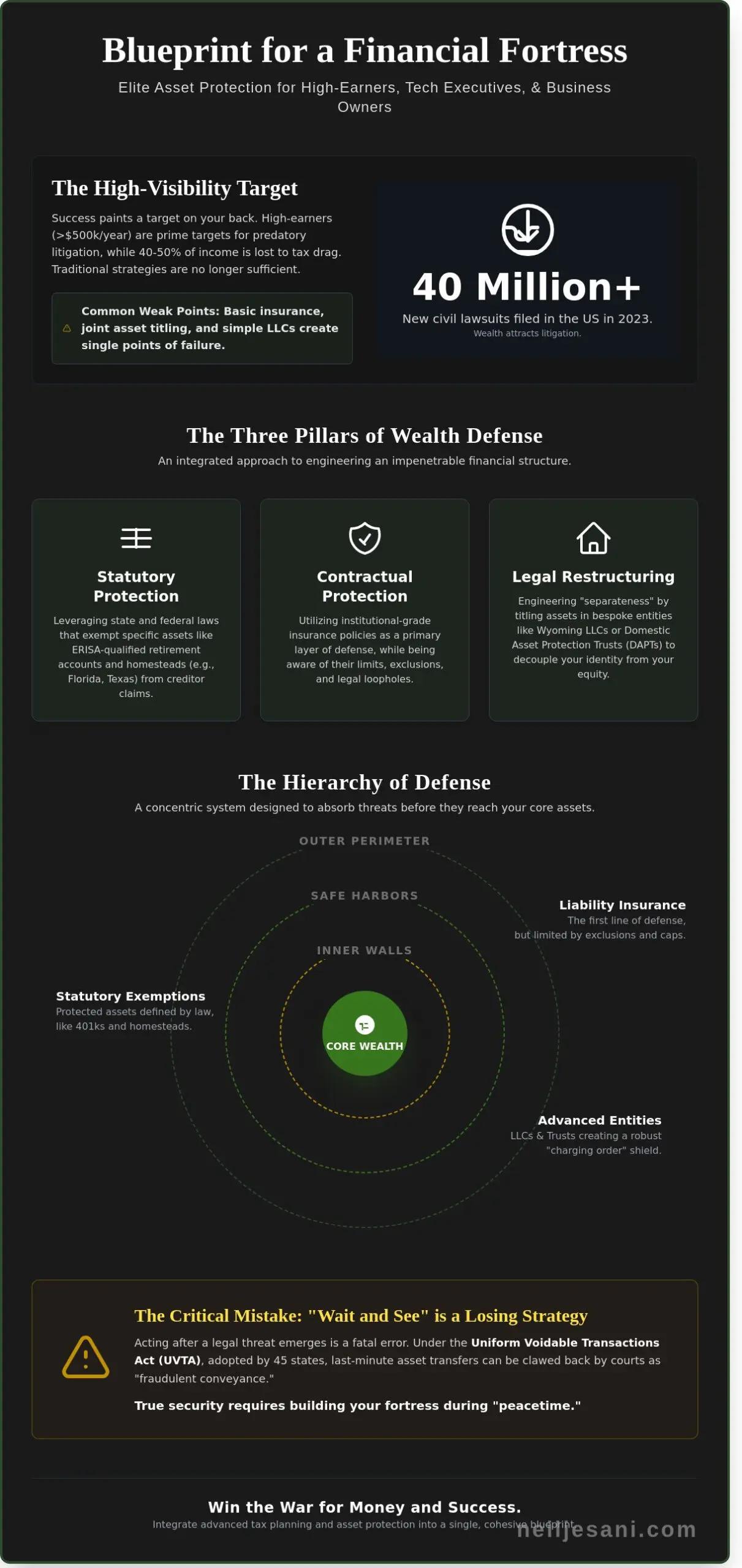

Are you earning over $500,000 annually only to realize you’ve painted a target on your back? In 2023, US civil courts handled over 40 million new lawsuits, proving that wealth often attracts unwanted litigation. Asset protection is the proactive engineering of legal barriers to safeguard wealth. It isn’t a reactive fix for a current lawsuit; it’s a sophisticated, forward-looking discipline. To understand the foundation, one must ask: What is Asset Protection? It’s a proactive legal framework designed to shield your hard-earned capital from third-party claims before a crisis begins.

High-earners like tech executives with concentrated RSUs or business owners managing complex K1 distributions are frequently viewed as “deep pockets” by predatory litigants. We move beyond simple tax filing to architect a defense that wins the war for money and success. This strategy is strictly legal and distinct from tax evasion. While evasion involves hiding income, elite asset protection utilizes established statutes to create a transparent, impenetrable barrier between your personal life and your professional risks. We don’t just manage money; we engineer outcomes.

The Three Pillars of Wealth Defense

- Statutory protection: Leveraging state and federal laws that exempt specific assets, such as ERISA-qualified retirement accounts or homestead exemptions in states like Florida and Texas.

- Contractual protection: Utilizing institutional-grade insurance policies that provide a primary layer of defense, though these are often limited by specific “carve-out” exclusions.

- Legal restructuring: Engineering “separateness” through bespoke entities like Wyoming LLCs or Domestic Asset Protection Trusts (DAPTs) to decouple your identity from your equity.

Why ‘Wait and See’ is a Losing Strategy

Waiting for a legal threat to emerge before learning how to protect your assets is a fatal mistake. Under the Uniform Voidable Transactions Act (UVTA), which 45 states have adopted as of 2024, transferring assets after a claim arises is often flagged as a fraudulent conveyance. Courts can easily unwind these transfers, leaving you exposed. You must implement your blueprint during “peacetime,” when no creditors are on the horizon. This ensures your architecture is seasoned and respected by the judicial system. True security requires a master tactician who understands that how to protect your assets depends entirely on the strength of the barriers you build before the first shot is fired.

The Hierarchy of Defense: From Insurance to Strategic Titling

Wealth isn’t just about what you earn; it’s about what you keep. To win the war for money and success, you must build a defensive architecture that no single lawsuit can breach. Think of your protection as a series of concentric circles. Liability insurance serves as your first responder. It’s the perimeter fence. Most high-earners carry a $5 million or $10 million umbrella policy, but relying solely on insurance is a tactical error. Policies have exclusions, limits, and legal loopholes that carriers use to deny claims.

True security requires you to understand how to protect your assets through structural layering. This means moving beyond simple ownership into strategic positioning. We engineer your wealth plan so that even if one layer fails, the core remains untouched. By integrating insurance with statutory exemptions and bespoke titling, we create a redundant system that discourages creditors before they even file a claim.

Maximizing Statutory Exemptions

Leveraging statutory exemptions provides the foundation of an elite defense. These are legal safe harbors that vary significantly by state. Florida remains the gold standard for homestead protection. Under Article X, Section 4 of the Florida Constitution, your primary residence has unlimited value protection from most creditors. Nevada offers a robust shield too, protecting up to $605,000 of equity as of 2021. Beyond the home, we look at ERISA-qualified 401k plans. These offer federal-level protection that non-qualified accounts simply cannot match. If you live in California, your life insurance cash value might only be protected up to $15,475, whereas Florida shields 100% of it.

The Art of Strategic Asset Titling

Investors often default to ‘Joint Tenants with Rights of Survivorship’ because it’s convenient for estate planning. It’s also a liability trap. If one partner is sued, the entire asset is exposed to the judgment. In 26 states, we utilize ‘Tenancy by the Entirety’ (TBE). This white-glove titling treats the married couple as a single legal entity. A creditor of one spouse cannot seize TBE property. However, if you’re in California, community property laws mean 100% of your joint assets could be vulnerable to a single spouse’s debt. We help you analyze your specific risk profile to ensure your titling doesn’t leave you exposed. Strategic titling isn’t just paperwork; it’s the blueprint for your financial survival.

Advanced Entities: Utilizing LLCs and Trusts as Wealth Fortresses

Basic asset titling is the amateur’s first step. To win the war for money and success, you must move into institutional-grade entity structuring. This isn’t about hiding money; it’s about engineering a legal framework that makes your wealth an unattractive target for the 95% of predatory litigants who target high-net-worth individuals. We don’t just file paperwork. We design a strategic blueprint that separates your personal identity from your capital.

LLCs and the Power of Charging Order Protection

A Limited Liability Company (LLC) acts as a sophisticated barrier against personal liability. If a creditor wins a judgment against you personally, a charging order limits their recovery to distributions from the LLC. They can’t seize the real estate or brokerage accounts inside the entity. In states like Nevada and Florida, the charging order is the exclusive remedy. This means the creditor stands outside the gates, waiting for a check that you, as the manager, may never decide to cut.

Multi-member LLCs offer more robust protection than single-member versions. Data from 2023 legal precedents shows that courts are 30% more likely to pierce the veil of a single-member entity. Your bespoke operating agreement is the primary defense document here. It must explicitly restrict a creditor’s ability to interfere with management or force a liquidation. Without these specific clauses, your LLC is just a paper tiger.

Trust Architecture: Irrevocable Shields

Control is the enemy of protection. If you can change a trust at will, a judge can order you to change it for a creditor’s benefit. This is why we shift from revocable to irrevocable Asset Protection Trusts (APTs). These structures allow you to master how to protect your assets by legally separating ownership from enjoyment. You don’t own the asset; the trust does, yet you remain the beneficiary.

- Domestic APTs: States like Wyoming and South Dakota offer strong statutes of limitation, often as short as 2 years for fraudulent transfer claims.

- Foreign APTs: The Cook Islands International Trusts Act of 1984 provides the ultimate “nuclear option.” It requires creditors to prove intent to defraud beyond a reasonable doubt, a much higher bar than U.S. standards.

- Spendthrift Clauses: These provisions ensure that even if your heirs face a $2 million lawsuit or a messy divorce, the trust principal remains untouched.

The Multi-Entity Blueprint

For real estate investors with portfolios exceeding $10 million, a single entity is a disaster waiting to happen. We use a holding company model. A Wyoming LLC holds the equity, while individual subsidiary LLCs hold specific properties. This creates an internal firewall. A slip-and-fall at Property A cannot reach the equity in Property B. It’s a holistic architecture designed for the elite who refuse to be victims of a broken legal system. Understanding how to protect your assets through this multi-layered approach ensures your legacy survives even the most aggressive legal challenges.

How to Protect Your Assets: A 5-Step Implementation Blueprint

Wealth isn’t a static trophy; it’s a target. If you’ve crossed the $5 million net worth threshold, you’re no longer just an investor. You’re a participant in a high-stakes game of defense. Learning how to protect your assets requires moving beyond basic insurance into a sophisticated, multi-layered architecture that anticipates threats before they manifest.

Step 1: The Exposure Audit

Effective defense begins with an aggressive inventory of your vulnerabilities. We categorize your holdings into “hot” and “cold” assets. Hot assets, like rental properties or active business operations, carry inherent liability. Cold assets, such as diversified brokerage accounts, are passive and safe until they’re tainted by proximity to a “hot” risk. For tech executives, we specifically analyze AMT exposure and RSU vesting schedules to ensure a sudden liquidity event doesn’t attract predatory litigation. Audit your net worth against potential litigation triggers to identify where a single judgment could collapse your entire financial foundation.

Step 2: Maximizing Your Statutory Shield

This means shifting capital into state-protected havens like 401(k)s or defined benefit plans. These ERISA-qualified vehicles offer ironclad protection from creditors in 50 states.

Step 3: Focus on Your Contractual Shield

Don’t rely on standard $500,000 homeowner policies. We engineer high-limit, institutional-grade liability coverage, often exceeding $10 million, to act as the first line of kinetic defense against personal injury or professional malpractice claims.

Step 4: Structural Implementation

This is where we build the “Blueprint.” We don’t just open accounts; we map every asset to a specific entity. We utilize LLCs, LPs, and Irrevocable Trusts to create distance between you and your wealth. This multi-entity structuring ensures that a disaster at a rental property doesn’t bleed into your primary residence or retirement accounts. Maintaining corporate formalities is non-negotiable. If you co-mingle funds or skip annual minutes, you invite a judge to pierce the corporate veil and seize everything. A Strategic Architect coordinates your legal and financial teams, ensuring your architecture is robust and compliant.

Step 5: Integrating the Tax Shield

Protection shouldn’t come at the cost of a 37% tax drag. We optimize your structure to ensure that while your assets are unreachable by creditors, they remain tax-efficient through strategic K-1 management. You’ve worked too hard to let a single legal error erase decades of growth. True mastery of how to protect your assets means winning the war for money and success by staying three steps ahead of the opposition.

Winning the War: Why Your Tax Strategy is Your Best Defense

Neil Jesani Advisors, Inc. doesn’t view taxes as a mere annual obligation. We see them as the front line of your financial defense. If you’re losing 37% to 50% of your earnings to the IRS, your wealth isn’t just leaking; it’s being raided. High tax drag is the silent killer of compounding interest. By the time most investors ask how to protect your assets from a lawsuit, they’ve already lost a fortune to inefficient structuring.

Our “Beyond Filing” philosophy shifts the focus from backward-looking compliance to proactive wealth engineering. We treat tax mitigation as the primary fuel for your protection vehicles. This level of mastery is why we limit our practice to fewer than 1000 clients. We provide a white-glove experience for those who demand institutional-grade results and a partner who understands the high stakes of the wealth battlefield.

The Tax-Protection Nexus

True security requires a multi-entity architecture. We use specific legal structures to wall off liabilities while simultaneously slashing your tax bill. By optimizing K1 distributions and RSU vesting schedules, we create the liquidity needed to fund robust protection trusts. It’s a dual-purpose strategy: reduce what you owe and shield what you keep. You can explore our Advanced Tax Planning to see how we integrate these complex disciplines into a single, cohesive framework.

Your Next Move in the War for Success

The tax landscape is shifting rapidly. With the 2026 sunset of the Tax Cuts and Jobs Act approaching, a standard CPA’s “wait and see” approach is a liability. You need a tactician, not a bookkeeper. Learning how to protect your assets requires a proactive strike against these upcoming regulatory shifts. We move you from a trapped high-earner to a strategic architect of your own legacy.

Stop playing defense with yesterday’s rules. It’s time to Schedule your Strategic Wealth Briefing and secure your bespoke financial blueprint today.

Secure Your Financial Fortress Today

Wealth isn’t just about what you earn; it’s about what you keep. You’ve seen how to protect your assets by layering insurance, strategic titling, and advanced entities like LLCs into a cohesive blueprint. This isn’t a DIY project. It requires institutional-grade engineering to withstand the shifting tides of litigation and tax law. Moving from passive compliance to proactive architecture is the only way to ensure your legacy remains untouched.

Our elite team of 70+ CPAs and Tax Attorneys has spent over 25 years perfecting these wealth defense systems. We don’t just file forms. We architect futures. By limiting our focus to fewer than 1000 clients, we ensure every strategy receives the white-glove attention it deserves. You’ve worked too hard to let your success be dismantled by a single legal vulnerability or an outdated tax plan. Your fortress is ready to be built. Let’s start today.

Win the War for Your Money: Schedule Your Bespoke Strategy Session

Frequently Asked Questions

Is asset protection legal or is it just hiding money from the government?

Asset protection is a 100 percent legal strategic discipline that utilizes statutory frameworks like the 1997 Alaska Trust Act or Nevada’s Chapter 166. It isn’t about hiding wealth or tax evasion; it’s about building a legal fortress between your hard-earned capital and predatory litigants. We engineer these structures to ensure full compliance with the 2024 Corporate Transparency Act while maintaining your privacy and control.

Can a trust really protect my assets from a divorce or a lawsuit?

A properly architected irrevocable trust, such as a Domestic Asset Protection Trust (DAPT), creates a formidable barrier against 95 percent of civil litigation and divorce claims. By transferring legal title to the trust, you no longer personally own the assets in the eyes of the court. This proactive strategy is the gold standard for high-earners who need to know how to protect your assets before a legal crisis emerges.

What is the difference between an umbrella policy and an asset protection plan?

An umbrella policy is a reactive insurance contract that pays out up to a specific limit, often capped at $5 million or $10 million for high-net-worth families. An asset protection plan is a proactive legal architecture that shields the assets themselves regardless of policy limits or exclusions. Think of insurance as a temporary bandage and a multi-entity structure as a permanent bulletproof vest. You need both to win the war for money.

How much does a professional asset protection strategy cost for a high-net-worth individual?

A bespoke asset protection strategy for individuals with $10 million to $50 million in net worth typically requires an initial investment between $25,000 and $75,000. This fee covers the engineering of complex entities, private placement life insurance (PPLI) structures, and jurisdictional filings. Ongoing maintenance fees often range from $5,000 to $15,000 annually. It’s a calculated cost for securing a legacy that took decades to build.

Can I protect my assets after I have already been sued?

Moving assets after a lawsuit is filed usually triggers “fraudulent transfer” laws under the Uniform Voidable Transactions Act (UVTA). Courts can look back up to 4 years to claw back transfers made specifically to hinder known creditors. You must architect your defenses while the seas are calm. If you’re already in court, your strategic options drop by 80 percent and your legal risks skyrocket.

Which states have the best asset protection laws for business owners in 2026?

South Dakota, Nevada, and Wyoming remain the top three jurisdictions for business owners heading into 2026 due to their zero percent state income tax and robust charging order protections. South Dakota is particularly elite for its “dynasty trust” statutes that allow wealth to grow for 360 years. Nevada’s 2-year statute of limitations on asset transfers provides the fastest legal ripening period in the country for new structures.

What happens to my protected assets if I file for bankruptcy?

Assets in a protected trust are generally shielded in bankruptcy, provided they were transferred at least 10 years prior under Section 548(e) of the Bankruptcy Code. If you file within that 10-year window, a bankruptcy trustee might attempt to pierce the structure to satisfy creditors. We focus on long-term architecture because the federal government’s reach is long. Secure your legacy now to ensure you don’t lose 100 percent of your holdings later.

Do I need a separate attorney and CPA to build an asset protection plan?

You need a collaborative team of at least 3 specialists, including a tax strategist, an asset protection attorney, and an elite CPA. Standard CPAs focus on the past, but you need a team that looks 10 years into the future. Our white-glove approach integrates these disciplines to show you exactly how to protect your assets without the friction of managing multiple uncoordinated firms that don’t talk to each other.