The 2026 Tax Landscape: Why Traditional Planning Leaves HNWIs Exposed

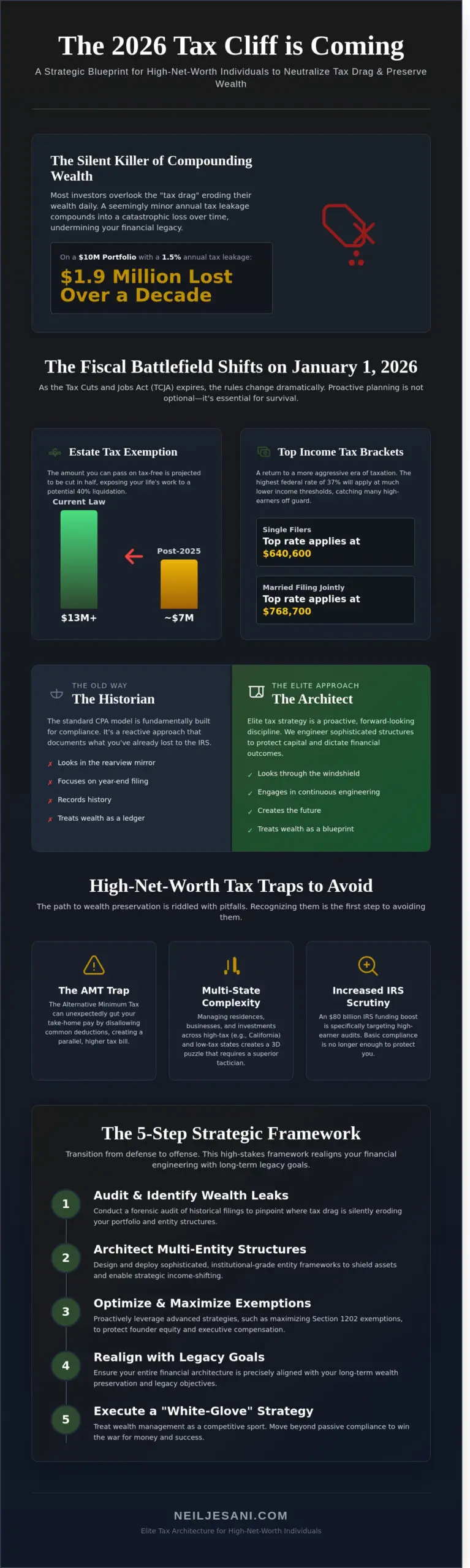

Most investors overlook the “tax drag” eroding their wealth every single day. On a $10M portfolio, a seemingly minor 1.5% annual tax leakage doesn’t just cost $150,000 this year. It compounds into a $1.9 million loss over a decade. This is the silent killer of compounding interest. For those seeking tax planning for high net worth individuals, the goal isn’t just to file accurately. It’s to eliminate the structural inefficiencies that treat your wealth like a public utility. We don’t just record history; we engineer the future to ensure you win the war for money and success.

The 2026 calendar year represents a massive shift in the fiscal battlefield. As the Tax Cuts and Jobs Act (TCJA) provisions sunset, we’re looking at top-tier tax bracket shifts that will catch many off guard. Single filers will see the top rate apply at $640,600; married couples filing jointly will hit that threshold at $768,700. These aren’t just incremental increases. They’re a return to a more aggressive era of taxation. Most high earners rely on the “Standard CPA Model,” which is fundamentally built for compliance. That model looks in the rearview mirror to report what you’ve already lost. We use legal tax reduction strategies to look forward, treating your balance sheet as a blueprint rather than a ledger.

Tax preparation is a commodity that any firm can provide. Tax engineering is a bespoke discipline. While a preparer asks for your 1099s in February, a strategic architect is moving pieces in October to ensure those 1099s reflect a lower liability. If your current advisor isn’t discussing multi-entity structuring or low-correlation alpha, they aren’t planning; they’re just documenting your losses to the IRS.

The High-Net-Worth Tax Trap

Wealthy families often fall into a trap where Alternative Minimum Tax (AMT) exposure and phased-out deductions gut their take-home pay. It’s a psychological shift you must make. You’re no longer in the business of “saving pennies” on your personal return; you’re in the mission of “protecting millions” across your entire enterprise. Advanced Tax Planning is a forward-looking wealth architecture rather than a year-end filing task. We focus on the institutional-grade maneuvers that keep your capital working for your legacy, not the federal government’s budget.

Why 2026 is a Pivotal Year for Wealth Preservation

The sunsetting of current tax laws means estate tax exemptions are projected to be cut in half, dropping from over $13 million per person to roughly $7 million. If you haven’t moved assets out of your taxable estate by December 31, 2025, you’re essentially volunteering for a 40% liquidation of your life’s work. This era of tax planning for high net worth individuals also requires a “White-Glove” advisory approach due to the IRS’s $80 billion funding boost specifically targeted at high-earner audits.

Complexity increases when you factor in a multi-state footprint. If you have a primary residence in Florida, tech holdings in California, and real estate in Nevada, your 2026 filing becomes a three-dimensional puzzle. You need a superior tactician to manage these jurisdictional overlaps. We provide the elite framework necessary to maintain your lifestyle while insulating your assets from an increasingly hungry tax system.

This puzzle becomes even more intricate for individuals with international ties, where navigating residency and visa issues is paramount. For those situations, coordinating with a professional immigration consultant Minneapolis is a key part of a comprehensive wealth protection strategy.

Engineering Wealth: Moving Beyond Compliance to Strategic Tax Architecture

Most CPAs spend their time looking in the rearview mirror. They record history; they don’t create it. For the ultra-wealthy, tax planning for high net worth individuals isn’t a seasonal task. It’s a continuous engineering project. At Neil Jesani Advisors, Inc., we act as the strategic architect. We build a comprehensive blueprint before you earn your first dollar of the year. This proactive stance ensures you aren’t just reacting to a bill. You’re dictating the terms of your wealth. We don’t just file forms. We design systems that protect your capital from unnecessary erosion.

Traditional wealth management is often built for the past. It relies on outdated models that ignore the complexity of modern income streams. Our approach is different. We view your financial life as a battlefield where taxes are the primary adversary. To win, you need more than a bookkeeper. You need a tactician who understands how to move assets across the board with precision. This is about flipping the script on the tax system and taking control of your financial destiny.

The Blueprint: Multi-Entity Design

A standalone individual is a target. A multi-entity structure is a fortress. We transition clients from simple ownership to institutional-grade frameworks that offer superior protection and efficiency. This involves using Family Limited Partnerships (FLPs), S-Corps, and complex Trusts to centralize management while decentralizing liability. While a standard filer pays the highest marginal rate, a multi-entity owner uses income shifting to move tax liabilities to lower-bracket entities. This strategy often centers on K-1 income and the rigorous optimization of Section 199A deductions. By maximizing the 20% pass-through deduction, we help business owners keep more of what they build.

Understanding IRS rules on estate and gift taxes is vital when building these structures. These entities must align perfectly with federal limits to avoid future audits or unintended tax triggers. Neil Jesani Advisors, Inc. specializes in these bespoke designs, ensuring your architecture is robust enough to withstand regulatory shifts. We focus on the future, not just the current filing season. If you want to see how an elite structure can change your trajectory, you can explore our strategic framework today.

Advanced Asset Location Strategies

Asset allocation tells you what to own. Asset location tells you where to put it. It’s the difference between a successful retirement and a tax-gutted legacy. High-growth assets with significant appreciation potential belong in tax-free buckets like Roth IRAs or specific trust structures. Conversely, low-correlation alpha or tax-inefficient bonds stay in taxable accounts where losses can be harvested to offset gains. This isn’t a minor detail. It’s a core component of tax planning for high net worth individuals who want to maximize every percentage point of growth.

Data shows that precise location optimization can increase after-tax returns by 1.2% to 1.8% annually. Over a 20-year horizon, that small margin is the difference between a $10 million portfolio and one worth over $14 million. We don’t guess with your future. We calculate. We ensure every dollar sits in the most tax-efficient home possible. By aligning your “what” with your “where,” we reduce the friction that taxes place on your compounding wealth. This is how the elite win the war for money and success.

High-Stakes Optimization: Advanced Vehicles for Income and Asset Protection

Most advisors react to your tax bill after the year ends. We engineer the outcome before the first vest date. For tech leaders and executives, equity is often the largest driver of wealth and the biggest source of tax leakage. Successful tax planning for high net worth individuals requires precision timing rather than simple compliance. We treat your balance sheet as a dynamic system that demands proactive defense.

Equity Compensation Mastery: RSUs and ISOs

If you hold Incentive Stock Options (ISOs), you face the “AMT Trap.” This occurs when the spread between the grant price and fair market value triggers a massive tax bill on paper gains you haven’t even liquidated yet. We mitigate this by calculating the exact number of options you can exercise without triggering the Alternative Minimum Tax. Early-stage executives must leverage the 83(b) election within 30 days of a grant to lock in a lower tax basis. Failing to plan for RSU vesting can lead to an immediate 37% federal tax hit plus state levies.

For founders and early investors in C-Corps, Section 1202 (Qualified Small Business Stock) remains the ultimate prize. If your shares qualify, you can exclude up to 100% of capital gains, capped at $10 million or 10 times your basis. We verify your company’s “active business” status and gross asset limits to ensure this exemption remains bulletproof when you exit.

Beyond traditional equities, we look for “Low-Correlation Alpha.” Institutional-grade portfolios utilize alternative investments like private credit and real estate to serve as tax-efficient wealth hedges. These vehicles provide:

- Accelerated Depreciation: Using cost segregation studies to create paper losses that offset real income.

- Tax-Deferred Growth: Utilizing 1031 exchanges or Opportunity Zones to reinvest gains.

- Structured K1s: Managing the flow of passive income to maximize deductions.

For many high-net-worth individuals, vacation properties in desirable locations are a key part of their real estate portfolio. Managing these assets effectively is crucial for both lifestyle enjoyment and investment returns; you can learn more about Northern Michigan Escapes to understand how specialized management can optimize such investments.

Strategic Philanthropy: Donor-Advised Funds and CRTs

We move our clients away from “checkbook charity” and toward “strategic philanthropy.” A Donor-Advised Fund (DAF) allows you to front-load five years of charitable giving into a single high-income year, securing an immediate deduction while you decide on distributions later. If you own highly appreciated assets with a low basis, a Charitable Remainder Trust (CRT) is a superior tool. It allows you to sell the asset tax-free, receive a lifetime income stream, and claim a significant charitable deduction. This strategy integrates perfectly with our framework for Asset Protection, ensuring your legacy is shielded from both the IRS and external liabilities.

The most common question we hear from ultra-high-earners is, “Is this legal?” This skepticism is healthy. Our strategies don’t rely on “grey area” offshore schemes or aggressive loopholes. Every blueprint we create is vetted by an elite team of CPAs and Tax Attorneys who understand the 70,000-page tax code. We don’t just file forms; we architect systems that stand up to the highest levels of scrutiny. You’ve spent decades winning the war for money. We provide the tactical expertise to ensure you keep it.

The 5-Step Framework for Reducing Tax Drag and Preserving Legacy

Stop treating your tax return like a historical record. It’s a strategic battlefield. Most high-earners lose 15% to 28% of their potential wealth to “tax drag” because they rely on reactive accountants who focus on compliance rather than engineering. We’ve developed a rigorous, institutional-grade framework designed to flip the script. This isn’t about simple deductions; it’s about winning the war for money and success through tax planning for high net worth individuals that anticipates shifts before they happen.

Our 5-step blueprint moves beyond the basics:

- Step 1: The Diagnostic Phase. We audit your last 3 years of filings to identify systemic wealth leakage. We look for the $100,000+ in missed opportunities that standard CPAs overlook in complex RSU or K1 structures.

- Step 2: Structural Engineering. We align your entities with your 2026 goals. This involves multi-entity “wall building” to protect assets and optimize flow-through income.

- Step 3: Tactical Implementation. We execute the blueprint with fractional CFO precision. Every move is measured against its impact on your total capital stack.

- Step 4: Continuous Optimization. We hold quarterly “insider” briefings. We don’t wait for year-end to adjust for market volatility or legislative changes.

- Step 5: Legacy Integration. We ensure your tax strategy supports your estate and succession plans, specifically preparing for the sunset of current exemptions on December 31, 2025.

Step 1 & 2: Finding the Leakage and Building the Wall

The diagnostic phase is where we uncover the truth about your current wealth management. While 90% of traditional firms only record what happened, our 70+ team members analyze how to change what *will* happen. We apply the “Power of Three”: we reduce taxes, build wealth, and design legacies simultaneously. This requires bespoke architecture. Cookie-cutter software cannot account for the nuances of concentrated stock positions or private equity distributions. We engineer a structural wall that separates your personal liability from your business growth while maximizing every available legal loophole.

The Ongoing Tactical Advantage

True tax planning for high net worth individuals requires a strategist on speed dial for every major financial decision. Our “Beyond Filing” approach means we operate like your personal family office. We provide the data needed for real-time pivots, especially as we approach the 2026 tax law shifts. Our white-glove quarterly review process includes a specific checklist to ensure no wealth is left on the table:

- Quarterly Cash Flow Audit: We analyze income timing to mitigate AMT exposure.

- Entity Compliance Check: We ensure multi-state nexus issues are managed to avoid double taxation.

- Legislative Impact Analysis: We model how the 2026 sunset affects your specific gift and estate thresholds.

- Alpha Correlation Review: We verify that your tax-loss harvesting aligns with your long-term investment alpha.

You shouldn’t be wondering if you’re overpaying. You should have the peace of mind that comes from a masterfully engineered system. If your current advisor hasn’t mentioned the $13.61 million exemption sunset, you’re already behind. It’s time to transition from a passive observer to a strategic architect of your own fortune.

Secure your financial future and engineer your bespoke tax strategy with our elite team of specialists.

The White-Glove Advantage: Why Elite Tax Strategy is a Competitive Sport

Wealth isn’t just a number on a screen; it’s a fortification. If you aren’t actively defending it, you’re losing the war for money and success. Most firms treat wealth management like a retail service. They chase volume, stack clients high, and offer diluted advice. Neil Jesani Advisors operates differently. We’ve intentionally limited our practice to fewer than 1,000 elite families and individuals. This isn’t about being exclusive for the sake of it. It’s about bandwidth. High-stakes financial engineering requires a level of focus that a 10,000-client firm can’t provide. We deploy a 70-person team where CPAs, Tax Attorneys, and Enrolled Agents sit at the same table. This unified front ensures your estate plan doesn’t conflict with your tax strategy, and your corporate structure doesn’t trigger unnecessary AMT exposure.

Mastering tax planning for high net worth individuals is a full-contact sport. You need a team that understands the nuance of K1s, low-correlation alpha, and multi-entity structuring. When your legal and tax professionals work in silos, you’re the one who pays for the friction. By bringing every discipline under one roof, we eliminate the “communication drag” that costs high-earners millions in lost opportunities. We don’t just file returns; we architect outcomes.

The Strategic Architect vs. The Commodity CPA

Are you a high-earner feeling trapped by your own success? Many W-2 executives with heavy RSU and ISO exposure find themselves paying 37% or more in federal taxes alone. A commodity CPA looks backward; they record history. They tell you what you owed last year. A Strategic Architect looks forward. We engineer strategies that go beyond filing. We possess a hunger for excellence that defines our culture. Stop settling for a tax preparer when you need a tactician. You’re invited to schedule an advanced tax strategy session to see the difference between compliance and true mastery.

Securing Your Legacy in a Post-2026 World

The clock is ticking toward December 31, 2025. When the current TCJA provisions sunset, the top individual rate is scheduled to jump back to 39.6%. The current gift and estate tax exemption, which sits at $13.61 million for 2024, could be slashed by nearly 50%. Effective tax planning for high net worth individuals requires acting now, not waiting for the 2026 deadline. Our white-glove promise is simple: peace of mind through total mastery of complex systems. We build blueprints that protect your legacy from legislative shifts and market volatility.

Your wealth deserves an architect, not just an accountant. It requires a partner who views tax efficiency as a competitive advantage. We provide the institutional-grade framework you need to flip the script on the tax system. Don’t let your hard-won success be eroded by standard advice. It’s time to move toward a bespoke strategy that reflects your ambition and secures your future. Winning the war for money and success starts with the right blueprint. Let’s build yours today.

Secure Your Financial Architecture Before the 2026 Sunset

The 2026 tax landscape isn’t a distant concern. It’s a looming shift that will redefine how you preserve your hard-earned capital. You’ve seen how traditional compliance fails to address the complexities of high-stakes wealth. By implementing our 5-step framework and utilizing advanced vehicles for asset protection, you move beyond simple filing into the realm of strategic tax architecture. It’s about engineering a blueprint that reduces tax drag and secures your legacy against shifting legislative tides.

Effective tax planning for high net worth individuals requires more than a standard CPA; you need a superior tactician. For over 25 years, we’ve specialized in wealth engineering for an exclusive circle of fewer than 1,000 clients. Our in-house team of CPAs, Tax Attorneys, and Enrolled Agents doesn’t just record the past. We design your future. You’ve built your empire through precision and grit. Don’t let outdated strategies erode your success. It’s time to deploy institutional-grade solutions that reflect your level of achievement.

Win the war for your money: schedule your Advanced Tax Strategy Session today.

You’ve earned your seat at the table, and we’re ready to help you protect it.

Frequently Asked Questions

What is the difference between tax planning and tax preparation for HNWIs?

Tax preparation is a backward looking compliance exercise while tax planning for high net worth individuals is a forward looking strategic architecture. Preparation focuses on the April 15 deadline and recording historical data to satisfy the IRS. Planning engineers your financial future to minimize liabilities before they occur. We don’t just record what happened; we design what will happen to ensure you keep more of your hard earned capital.

How much can a high-net-worth individual realistically save through advanced planning?

High net worth individuals can realistically reduce their effective tax rate by 10% to 25% through advanced strategic engineering. For a household earning $2 million annually, this translates to $200,000 or more in annual tax alpha. These savings aren’t accidental. They result from optimizing RSU vestings, utilizing private placement life insurance, and restructuring multi-entity business holdings to capture every available credit.

Is advanced tax planning legal and compliant with the IRS?

Advanced tax planning is 100% legal and relies on the 6,000 plus pages of the Internal Revenue Code to protect your wealth. We operate strictly within the boundaries of IRS regulations and established judicial precedents. Our strategies use the same frameworks employed by Fortune 500 companies to optimize their balance sheets. You aren’t evading taxes; you’re exercising your right to pay the minimum amount required by law through superior architecture.

What is the “AMT Trap” and how do I avoid it in 2026?

The AMT Trap refers to a parallel tax system that triggers when certain deductions are too high, and it’s set to capture more taxpayers after the TCJA provisions expire on December 31, 2025. You avoid it in 2026 by managing the timing of ISO exercises and state tax payments. We monitor your income thresholds to ensure you don’t cross the $1,000,000 phase out limit where exemptions vanish and tax rates spike.

How does multi-state residency affect my tax planning strategy?

Multi-state residency creates a complex web of tax “nexus” that can lead to double taxation if you don’t track your 183 day physical presence meticulously. States like California and New York aggressively audit high earners who claim residency elsewhere. We build a robust evidentiary trail to prove your primary domicile. This includes tracking travel logs and utility bills to ensure your tax planning for high net worth individuals remains bulletproof against state revenue agencies.

When should a business owner start exit planning for tax purposes?

Business owners should start exit planning at least 36 to 60 months before a liquidity event. This timeline allows for the implementation of Qualified Small Business Stock (QSBS) strategies under Section 1202, which can exclude up to $10 million in capital gains. If you wait until the Letter of Intent is signed, you’ve likely lost 80% of your tax saving opportunities. Early architecture ensures your legacy remains intact.

What are the best tax-advantaged accounts for earners making over $500k?

Earners making over $500,000 should prioritize Cash Balance Plans and Private Placement Life Insurance (PPLI) to shield income from immediate taxation. A well structured Cash Balance Plan can allow for tax deductible contributions exceeding $200,000 annually depending on your age. These institutional-grade tools provide a level of tax deferral and asset protection that standard 401ks simply can’t match. We engineer these blueprints to maximize your long term wealth.

How do Neil Jesani Advisors differ from a traditional wealth management firm?

Neil Jesani Advisors operates as a boutique strategy firm that limits its practice to fewer than 1,000 elite clients to ensure a true white-glove experience. Traditional firms are often reactive and built for the masses, focusing on generic asset allocation. We act as your Strategic Architect, leading a proactive mission to win the war for money and success. Our team of 70 plus professionals focuses on the future, not just the filing.