Your current CPA is likely a historian, not a strategist. While they accurately record what happened last year, they are often silent about the $250,000 you are losing annually to unnecessary tax drag. If you only hear from your advisor during tax season, you are already losing the war for money and success. Identifying the signs you need a new CPA is the first step toward securing an institutional-grade financial blueprint. You deserve a partner who engineers outcomes rather than one who simply reports them. Most high-earners don’t realize they’re overpaying by 15% or more because their current firm lacks the sophistication to look beyond basic filing.

It’s exhausting to feel like just another number in a massive corporate machine while your wealth remains exposed. You expect your advisor to be a proactive advocate for your legacy, yet you’re often left with reactive communication and “off the shelf” advice. This article will show you how to distinguish between a compliance officer and a strategic architect. We’ll explore the seven red flags that prove your current advisor is costing you millions; then, we’ll outline the path to a bespoke, white-glove tax architecture designed for elite wealth protection.

Key Takeaways

- Distinguish between a “historian” who merely records the past and a “strategic architect” who engineers your future to eliminate unnecessary tax drag.

- Identify the high-stakes red flags and signs you need a new CPA, ensuring your advisor is focused on your long-term legacy rather than just April deadlines.

- Quantify the invisible cost of mediocrity by learning how a 2% difference in tax efficiency can compound into millions of lost wealth over a 20-year horizon.

- Master the “Upgrade Blueprint” to vet an elite tax team, demanding a three-year retrospective review and an integrated framework of attorneys and CPAs.

- Discover how to transition to a “white-glove” experience where 70+ in-house tacticians proactively protect your wealth and win the war for money and success.

Tax Filer vs. Tax Strategist: Which One Are You Paying For?

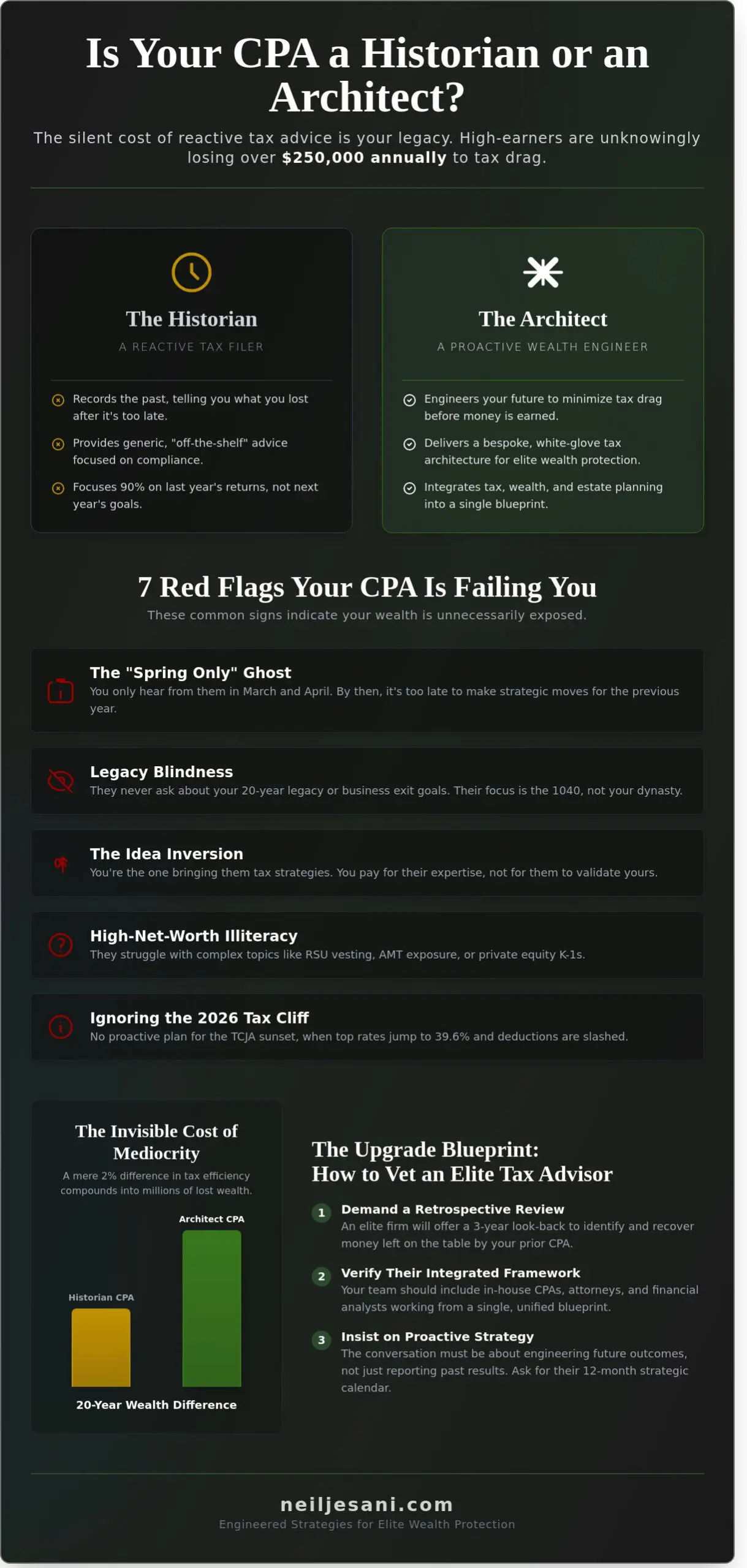

Most high-earners are trapped in a rearview mirror relationship with their financial professionals. They pay for a Historian. This type of accountant records what happened last year, organizes your receipts, and ensures your forms reach the IRS on time. While a Certified Public Accountant (CPA) is technically qualified to perform these tasks, a Historian only documents your wealth’s attrition. They tell you how much you lost to the system after it’s too late to change the outcome.

The Architect CPA operates on a different plane. This professional is a wealth engineer who builds structures to minimize tax drag before the money is even earned. They don’t just report income; they design the environment in which that income exists. If your current advisor spends 90% of their time talking about last year’s returns and 10% on next year’s goals, it’s one of the clearest signs you need a new CPA who understands the urgency of the 2026 tax landscape.

On January 1, 2026, the provisions of the Tax Cuts and Jobs Act are scheduled to sunset. This isn’t a minor adjustment. Top individual tax rates are projected to jump from 37% back to 39.6%, and the standard deduction will be nearly cut in half. High earners cannot afford compliance-only accounting when the federal government is preparing to take a significantly larger bite of their balance sheet. Your tax return should be the final, quiet confirmation of a year-long strategy, not a stressful surprise delivered every April.

The Compliance Trap

Clean books are the bare minimum. They aren’t the goal. Many professionals fall into the trap of believing that avoiding an audit is the ultimate success. This reactive mindset is dangerous for tech executives and business owners. When accounting is purely reactive, you miss the critical 90-day windows required to optimize ISO exercises or manage RSU vesting schedules effectively. Staying with the “everything looks fine” status quo often costs families millions in lifetime wealth because they failed to act before a liquidity event occurred.

The Anatomy of Advanced Tax Planning

Advanced Tax Planning moves the conversation from “What do I owe?” to “How do we engineer a different result?” It requires integrating tax strategy directly with wealth management, estate planning, and risk mitigation. You shouldn’t have three different professionals giving you three different answers. You need a single blueprint that coordinates your corporate entities, your private foundations, and your personal portfolios to ensure every dollar is working toward your legacy.

Advanced Tax Planning is a proactive, multi-entity engineering process. It functions as a sophisticated framework that aligns your legal structure with your long-term financial objectives to maximize capital retention.

Winning the war for money and success requires a tactician who looks five moves ahead. If you’re still waiting for your accountant to call you with an idea, you’ve already lost the initiative. Recognizing the signs you need a new CPA is the first step toward moving from a defense-only posture to an elite, offensive strategy that protects your hard-earned capital for generations to come.

7 Signs Your Current CPA Is Failing Your Wealth

Most high-earners treat tax season like a recurring root canal. It is painful, it is annual, and it is over as quickly as possible. If your advisor functions as a historian rather than a strategic architect, you are losing money every single day. A standard accountant records the past; a wealth strategist engineers the future. Recognizing the signs you need a new CPA early can save you hundreds of thousands in avoidable “tax drag” over a decade.

- The “Spring Only” Ghost: You only hear from them in March and April. By the time they look at your numbers, it is too late to move the needle.

- Legacy Blindness: They never ask about your business exit goals or your 20-year legacy plan. They are focused on the 1040, not the multi-generational estate.

- The Idea Inversion: You are the one sending them screenshots of tax strategies you found on LinkedIn or heard from peers at the club. You are paying them for their expertise, not for them to Google yours.

- HNW Illiteracy: They struggle with high-net-worth triggers like Alternative Minimum Tax (AMT) exposure, complex K-1s from private equity, or RSU vesting schedules.

Wealth is not a static number. It is a dynamic system that requires constant calibration. If your current professional is not looking for ways to flip the script on the tax code, they are not an ally; they are a compliance clerk. Before you commit to a new partnership, always verify a CPA’s license through official state boards to ensure they maintain the necessary credentials for high-stakes advisory.

Communication and Proactivity Gaps

The “Ghosting” red flag is more than an annoyance. Waiting three weeks for a response on a mid-year asset purchase can cost you a 100% bonus depreciation opportunity. Elite wealth management requires a “white-glove” service level where your advisor initiates the strategy. If they aren’t calling you by July 15th to run a mid-year projection, they aren’t managing your wealth. They are just surviving their own workload. High-volume firms often operate on a “churn and burn” model that leaves no room for the deep work required for bespoke tax architecture.

Technical Stagnation in a 2026 Landscape

The tax world is facing a massive shift. The Tax Cuts and Jobs Act (TCJA) provisions are set to sunset on December 31, 2025. If your CPA is still using 2018 strategies for a 2026 regulatory environment, your wealth is at risk. We are moving from a period of relative tax stability into a high-volatility era where the top bracket is expected to jump back to 39.6%.

Stagnant CPAs also fail to address multi-state nexus issues. In our remote-first world, an executive working from a vacation home in a high-tax state for more than 183 days can trigger a massive, unexpected tax bill. Finally, beware of the “No” Reflex. Many accountants say no to complex strategies like captive insurance or advanced trust structures simply because they don’t understand them. They prioritize their own comfort over your capital. This is one of the clearest signs you need a new CPA who understands the architecture of elite wealth.

The Invisible Cost of a Mediocre CPA

One of the most dangerous signs you need a new CPA is the quiet presence of “Tax Drag.” This isn’t a single error on a form; it’s a systemic leak where a 2% or 3% gap in tax efficiency compounds into a catastrophic loss of capital over time. Most high earners mistake a “fast” CPA for an efficient one. They celebrate a quick filing while ignoring the reality that their accountant is a historian, not a strategist. If your current provider only looks backward at what you spent rather than forward at what you can save, you’re paying a hidden tax on your own growth.

The risk extends beyond the balance sheet. Poor documentation in a high-volume, “fast” firm creates a paper trail of sand. When the IRS initiates an audit, the lack of rigorous, institutional-grade documentation transforms a routine inquiry into a multi-year legal battle. You don’t just lose money in these scenarios; you lose the ability to focus on your primary mission of building your enterprise. When choosing the right CPA, you must demand a partner who engineers strategies to withstand scrutiny rather than one who merely fills out boxes to meet a deadline.

Compounding Losses in Wealth Preservation

Consider a hypothetical breakdown of a high-performing executive earning $500,000 annually. Without a bespoke tax blueprint, this individual often loses $30,000 every year to avoidable inefficiencies like poor entity selection, missed QBI deductions, or unoptimized RSU vesting schedules. If you overpay your tax bill by $25,000 every year for two decades, you aren’t just losing $500,000 in nominal cash; you’re forfeiting over $1.02 million in potential wealth when factoring in a 7% compounded annual return. This is the price of mediocrity. Beyond the math, missing asset protection layers can be even more devastating. A single lawsuit against an unprotected entity can wipe out ten years of disciplined gains in a single afternoon. We design frameworks that protect, preserve, and propel your capital simultaneously.

The Stress of “Self-Advising”

High earners often fall into the trap of “self-advising,” which is a clear indicator of a failing professional relationship. If you find yourself spending your weekends reading IRS Bulletins to verify your accountant’s work, these are the definitive signs you need a new CPA who operates at your level. The mental load of double-checking a professional is a weight you shouldn’t carry. Your time is worth thousands of dollars per hour. Every minute you spend debating tax code minutiae is a minute stolen from your business growth or your family legacy. True peace of mind comes from institutional-grade oversight where the strategy is proactive, the execution is flawless, and the burden of knowledge rests entirely on your advisor’s shoulders.

This principle of leveraging expert support extends beyond finance. Busy executives in the Minneapolis-St. Paul area, for example, understand that reliable airport transport is non-negotiable for high-stakes business travel, often relying on specialists like Edina Taxi MN to ensure efficiency and peace of mind.

Is the hassle of switching worth the potential savings? Many business owners hesitate because they fear the transition process. However, the cost of staying with a mediocre firm is an infinite liability. Consider these three factors:

- The Opportunity Cost: A single missed R&D credit or a poorly structured real estate professional status (REPS) claim can cost more than ten years of accounting fees.

- The Audit Shield: Elite firms provide a level of documentation that discourages aggressive audits before they even begin.

- The Growth Multiplier: A strategic architect identifies capital you didn’t know you had, allowing you to reinvest in your most profitable assets.

The transition to a boutique, high-value firm is a one-time investment in a lifetime of structural efficiency. Don’t let the fear of a few hours of paperwork prevent you from reclaiming millions in lost wealth.

The Upgrade Blueprint: How to Vet an Elite Tax Advisor

Transitioning away from a legacy relationship is a high-stakes tactical move. If you’ve identified the signs you need a new CPA, your next step isn’t just to find a replacement; it’s to secure a strategic architect. You aren’t looking for a historian who records what happened last year. You need a forward-looking tactician who engineers your financial future. This blueprint ensures your next firm is equipped to win the war for your money and success.

- First, demand a forensic review of your last 36 months of returns. An elite advisor doesn’t just glance at your 1040. They perform a deep-tissue scan of your previous filings to identify missed deductions, improper RSU treatment, or overlooked multi-entity opportunities. It’s common for our team to find $50,000 to $250,000 in recapturable value that “standard” firms simply ignored.

- Look for an integrated powerhouse. Boutique firms that house CPAs, Attorneys, and EAs under one roof provide a 360-degree shield. When your tax strategy is divorced from your legal structure, you’re vulnerable. You need a unified front where every tax move is legally fortified and strategically sound.

- Verify niche mastery. If you’re a tech executive with complex ISOs or a real estate mogul with 1031 exchanges, a generalist is a liability. Demand specific case studies from your industry. A firm with 25 years of experience in high-stakes niches will understand the nuances of AMT exposure and K1 distributions better than a neighborhood tax preparer.

- Evaluate “Strategic Hunger.” Does the firm wait for your call, or do they hunt for savings? An elite advisor possesses a relentless drive to optimize. They should be more aggressive about protecting your wealth than you are.

- Confirm fiduciary status and white-glove service. Your advisor must be a 100% fiduciary, legally bound to put your interests first. This isn’t a suggestion; it’s a requirement for institutional-grade wealth protection.

Finding a firm that embodies these principles is crucial. As an example of this integrated approach, firms like Timothy Roberts & Associates, LLC combine comprehensive wealth management with strategic tax solutions to provide the kind of unified oversight that high-earners require.

Questions to Ask During the Interview

Ask how many clients the firm serves. The “fewer than 1,000 clients” benchmark is critical. If a firm handles 5,000 clients, you’re a number in a machine. You want a boutique environment where you receive bespoke attention. Inquire about their proactive strategy for the 2026 tax sunsets. If they don’t have a specific framework for the expiration of the Tax Cuts and Jobs Act (TCJA) provisions, they’re already behind. Finally, ask how they integrate your investment portfolio with your tax plan to ensure low-correlation alpha and maximum net returns.

The Onboarding Experience

The transition to a high-level firm should be painless. A sophisticated “Discovery Phase” involves more than just a document upload. It’s a strategic briefing where the firm maps out your multi-entity architecture and identifies immediate “quick wins” for the current fiscal year. This is where you distinguish the “Strategic Architect” from the “Data Entry Clerk.” An elite firm takes the lead, coordinating with your previous CPA to transfer files so you can focus on your business. They don’t just file forms; they design legacies. If your current professional doesn’t meet these standards, it’s one of the clearest signs you need a new CPA who can provide an institutional-grade framework.

Stop settling for reactive tax filing and start engineering your wealth strategy today. Partner with an elite tax advisor at NeilJesani.com

Neil Jesani: Engineered Strategies for the Elite 1000

Standard tax preparation is a commodity. If you recognize the signs you need a new CPA, you’ve likely outgrown the reactive model of filing and forgetting. At Neil Jesani Advisors, Inc., we don’t just record history; we engineer the future. Our firm provides a white-glove experience designed for high-net-worth families who demand more than a math checker. We’ve built an in-house team of 70+ tacticians who operate with a single mission: to protect your balance sheet from unnecessary erosion. This isn’t a traditional accounting office. It’s a war room where 200 years of combined heritage meets aggressive, forward-looking strategy.

We intentionally limit our practice to fewer than 1,000 clients. This exclusivity isn’t just a marketing tag; it’s a functional requirement for the level of precision we provide. When a firm manages 5,000 files, you’re a number lost in the shuffle of tax season. When you’re one of our Elite 1000, you have a dedicated architecture for your wealth. We apply the “Win the War for Money and Success” philosophy to every line item. This means treating taxes as a controllable expense rather than an inevitable burden. We look at your total financial picture to ensure your wealth is working as hard as you did to earn it.

Bespoke Wealth Preservation

Traditional CPAs often struggle with the friction of modern, complex wealth. We specialize in the heavy lifting that stops typical accountants in their tracks. Whether you’re managing complex K-1 distributions from private equity, navigating RSU ladders, or optimizing ISO exercises, our team builds the framework to capture every cent. We implement institutional-grade asset protection strategies that 95% of retail CPAs ignore. For example, we helped a tech executive with a $2.4 million annual income flip the script on their tax bill last year. By restructuring their multi-entity holdings and optimizing their deferred compensation, we reduced their effective tax rate by 14% in a single cycle. We focus on low-correlation alpha and AMT exposure to ensure your legacy remains intact.

Take the Next Step

The most expensive mistake you can make is waiting until April to think about January. If you’ve identified the signs you need a new CPA, the clock is already ticking on your current year’s savings. Most high-earners lose $50,000 to $150,000 annually simply because their current accountant is looking in the rearview mirror. We invite you to an Advanced Tax Strategy Session to see the difference between a preparer and a strategist. This isn’t a generic consultation; it’s a deep dive into your financial architecture to find the leaks in your current plan. Stop settling for a defensive posture. It’s time to play offense with your capital. Schedule your strategy session with Neil Jesani Advisors, Inc. today and secure your financial future.

Take Command of Your Wealth Architecture

Your current advisor might be a master of the past, but wealth preservation requires a master of the future. If you’ve recognized the signs you need a new CPA, you’re already ahead of the curve. A standard tax filer records history; a strategic architect engineers it. Every year you spend with a mediocre advisor isn’t just a service fee. It’s a multi-million dollar tax leak that erodes your legacy. You deserve a team that operates with institutional-grade precision and a proactive mindset.

Neil Jesani provides a white-glove experience backed by a powerhouse team of 70+ CPAs, Tax Attorneys, and Enrolled Agents. We don’t settle for “good enough” because we’ve spent 25+ years refining financial engineering for the world’s most successful individuals. We deliberately limit our practice to fewer than 1,000 elite clients to ensure every strategy is bespoke. It’s time to stop paying for basic compliance and start investing in a blueprint that wins the war for money and success. You’ve worked too hard to let outdated strategies drain your accounts.

Secure your wealth with an Advanced Tax Strategy Session. Your empire deserves an elite tactician.

Frequently Asked Questions

Is it difficult to switch CPAs in the middle of the year?

Switching CPAs mid-year is a seamless process that often yields a 20% increase in tax efficiency before the December 31 deadline. You don’t need your current accountant’s permission to move your files; you simply authorize the digital transfer of your records. Making the move by September 30 allows a new strategist to implement Q4 maneuvers that a standard tax preparer would miss during the spring rush.

What is the difference between tax preparation and tax planning?

Tax preparation is a backward-looking administrative task, while tax planning is the proactive engineering of your financial future. If your current advisor only speaks to you in April, these are clear signs you need a new CPA who focuses on architecture over reporting. We look at the next 10 years of your legacy, not just the last 12 months of your expenses, to ensure you keep more of what you earn.

How much should a high-net-worth individual expect to pay for a top-tier CPA?

High-net-worth individuals should expect to invest between $5,000 and $50,000 annually for elite, strategic representation. This isn’t a cost but a capital allocation toward wealth protection. When you’re managing $10 million or more in assets, a fee representing 0.5% of your total tax savings is a standard benchmark for institutional-grade service. You’re paying for a tactician who wins the war for your money.

Can a new CPA find mistakes or missed deductions in my previous years’ returns?

A new strategist can review and amend your returns from the last 3 years to recover overpaid taxes. We frequently identify missed opportunities in multi-entity structuring or RSU cost-basis reporting that result in 6-figure refunds for new clients. This forensic approach ensures you aren’t leaving your hard-earned capital in the hands of the IRS due to past clerical oversights or passive advice.

Does a boutique firm offer the same protection as a “Big 4” accounting firm?

Elite boutique firms often provide superior protection because they limit their roster to fewer than 1000 clients to ensure deep, personalized oversight. While a “Big 4” firm treats you as a line item, a boutique strategist engineers a bespoke framework for your specific AMT exposure and K1 complexities. You get institutional-grade expertise without the diluted attention or high turnover found in a massive corporate machine.

What documents should I have ready when interviewing a new tax strategist?

You should prepare your last 3 years of federal and state tax returns, all current K-1s, and your most recent 1099s. Bringing your business entity organizational charts and RSU vesting schedules allows a tactician to identify immediate structural leaks. These documents provide the blueprint we need to flip the script on your current tax liabilities and design a more efficient wealth architecture.

How does the 2026 tax law change affect my need for a new advisor?

The sunset of the Tax Cuts and Jobs Act on January 1, 2026, means tax brackets will revert to higher levels, making current planning critical. If your advisor hasn’t discussed how the 37% top rate might jump back to 39.6%, these are signs you need a new CPA immediately. You have less than 24 months to restructure your estate and income streams before the window for current exemptions closes forever.